Часть I: Биткойн как дерево, настойчивость и глубокие структуры

Мечтание

Возможно, если Я был более наглым, название первой части этой серии закончилось бы чем-то более соблазнительным, чем-то резким, вроде «Биткойн-это пальма, а фиат-это кокос». Но, что бы там ни было, такое название казалось слишком легкомысленным, слишком тропическим и тривиальным для такой весомой темы.

По правде говоря, изображение пальмы на самом деле было бы очень точным аллегория того, как будет развиваться дорожная карта биткойнов и фиатных денег по мере нашего продвижения в 21 век. Королевская пальма roystonea oleracea лихорадочно покачивается в сильном шквале, но никогда не перестает крепко держаться за свои корни глубоко под землей. И, как и в случае с любой бурей, единственная дарвиновская необходимость для этого дерева-это выживание, чтобы выжить в буре как можно более невредимым.

Другие деревья и строения могут расколоться и сломаться в капитуляции перед суровыми капризами природы, оставив больше солнечного света для нашей королевской ладони, чтобы поглотить, когда небо очистится. Обломки всего, что не было достаточно прочным, чтобы пережить нападение, метаболизированные колониями термитов и кустарниковыми пожарами, превратились в пышную и плодородную почву. Новый базовый слой для восстановления и процветания. Удачная метафора в свете того факта, что почва оказалась единственной физической средой, когда-либо наблюдаемой в природе, способной превратить смерть в жизнь. Точно так же абсолютно дефицитные, неподкупные здоровые деньги-это единственная экономическая среда, способная вдохнуть экономическую жизнь в разлагающуюся и деградировавшую финансовую систему.

Предупреждение

«Безвредная передача ваших время на лугах вдали

Только смутно осознаю некоторую тревогу в воздухе

Тебе лучше остерегаться

Здесь могут быть собаки

Я посмотрел на Джордан и увидел

Вещи не такие, какими кажутся

Что вы получаете, притворяясь, что опасность не настоящая

Кроткий и послушный, вы следуете за лидером.

По проторенным коридорам в стальную долину

Какой сюрприз!

Выражение смертельного шока в вашем глаза

Теперь все действительно то, чем кажется

Нет, это неплохой сон »

-Роджер Уотерс,« Овца », 1977 г.

Источник: Нарита Мартин, @R

Пророчество

«Вы слышали о розе, которая выросла из трещины в бетоне?

Доказав неверность законов природы, она научилась ходить без ног.

Забавно, это было кажется, сохраняя свои мечты, он научился дышать свежим воздухом.

Да здравствует роза, выросшая из бетона, когда никому даже не было до этого дела ».

-Тупак Шакур,« Роза, выросшая из бетона , »1999 г.

Прежде чем мы сможем в полной мере оценить характеристику стойкости биткойнов, о которой говорилось выше, возможно, будет полезно контекстуализировать, как и почему такая «антихрупкость» (что мы определим более подробно ниже) неизбежно проявляется как раскат грома, пощечина лицо, позволяющее всем нам увидеть его глубоко недооцененную полезность.

Чтобы добиться этого, давайте сделаем небольшой обходной путь, используя модифицированную версию методики Сократова вопросов.

Теория: паническое бегство класса массовых инвесторов

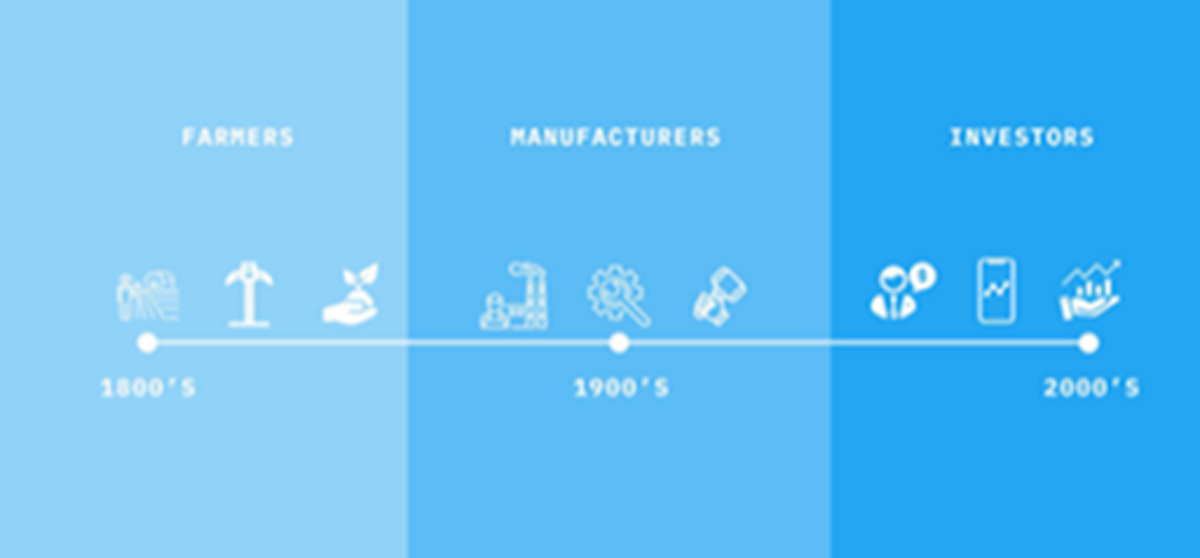

Уважаемый политический инвестор в технологии Баладжи Сринивасан в своей концептуальной модели децентрализованной псевдонимной экономики противоречиво заявил:

«В 1800-х годах все были фермерами. В 1900-х все занимались производством. В 2000-х каждый становится инвестором… И одна из вещей, которую люди не понимают, пока не станут инвесторами,-это идея о том, что денег много ».

-Баладжи Сринивасан,« Инвестируйте как лучший подкаст с Патриком О’Шонесси »

Источник: Баладжи Сринивасан

A Обсуждение

Давайте примем вышеприведенное утверждение за чистую монету и примем его на данный момент как развивающуюся априорную реальность. Я думаю, что большинство из нас согласятся с тем, что такое расширение охвата класса инвесторов действительно быстро набирает обороты, особенно в постпандемическом мире. Трудно отрицать веские доказательства (обсуждаемые ниже), а также наблюдаемое культурное внимание, которое делает упор на самостоятельное инвестирование на фондовом рынке. Доказательства повсюду, даже прокручивая мою ленту новостей, когда я писал это эссе:

«Robinhood работает над функцией, позволяющей пользователям вкладывать лишние изменения»

«Вложение лишних сдач имеет становится все более популярной стратегией для новых биржевых трейдеров и является ключевым элементом конкурирующих приложений, таких как Acorns, Chime и Wealthsimple ».

Поскольку символическое IPO Robinhood теперь врезалось в нашу недавнюю память, заголовки, указанные выше, являются прекрасным примером для нашего обсуждения. Микрофинансирование на фондовом рынке станет олицетворением этой эволюции в сторону массового инвестора. Я, например, вижу эти изменения вокруг себя, в моей профессиональной жизни в индустрии хедж-фондов, в культуре растущего FOMO, жадности и беспокойства, вплоть до моего личного взаимодействия с друзьями и семьей и в социальных сетях. Я даже считаю, что это то, что многие политики и технократы сознательно стремятся стимулировать. И это меня беспокоит.

Каковы последствия такой социальной трансформации? И каковы его коренные причины?

Такие открытые вопросы, возникающие в результате этого наблюдения,-одна из причин, почему меня так привлекает и заинтригована гипотеза Шринивасана. Его заявление открывает дверь для множества дискуссий и затрагивает некоторые очень важные темы.

Некоторые из этих тем, относящихся к неизбежности децентрализованной экономики,-это темы, которые будут обсуждаться более подробно во второй части этой серии. А пока давайте подготовим почву, поняв, почему поощряется массовый класс инвесторов, как это приведет к еще большей централизации и как все эти открытые двери представляют собой односторонние эскалаторы, гарантированно приведшие к дальнейшим деревьям решений, зависящих от пути. , и в конечном итоге порождают почти бесконечную нестабильность и системную хрупкость.

И то, что станет предельно ясно, так это целостное взаимодействие между неизбежностью и неустойчивостью этого пути на одной стороне медали. А затем настойчивость биткойна с другой стороны, терпеливо ожидающая своей очереди, чтобы подняться в воздух, неистово вращаясь, хотя и спокойная и собранная, терпеливо ожидая приземления лицом вверх.

Метафора сэндвича

Пророчество Сринивасана неосознанно раскрывает реальность опасного переходного периода, в котором сейчас находится мировая экономика. Сейчас мы находимся в запутанном состоянии неопределенности, ненадежно зажатой между децентрализацией и централизацией.

Культурная энергия этого текучего временного состояния, безусловно, вызывает определенное «беспокойство в воздухе», хотя растущее недовольство ощутимо. И точно так же, как события пандемии COVID-19 вызвали усиление многих тенденций, одна из этих тенденций действительно является проявлением «пролетариата» и агрессивно расширяющегося класса инвесторов. И хотя у такого прогресса есть много положительных качеств-начиная от самовыражения, возможности для создания нового богатства в краткосрочной перспективе и финансового образования в области рынков, управления рисками, денег и экономической теории-все такие преимущества, к сожалению, ошибочны и недолговечны. зрячий. В конце концов, эти весьма ощутимые выгоды должны быть разбавлены и побеждены зловещими силами.

Основные причины того, почему коммерциализация класса инвесторов является такой опасной эволюцией, в первую очередь могут быть связаны со сроками, исторический контекст и последствия того, что потребуется этому сообществу массовых инвесторов в форме второго и третьего производных эффектов.

Пожалуйста, проявите терпение ниже, поскольку этот первый раздел неизбежно изобилует некоторыми финансовыми данными и терминологией. Однако такие данные необходимы, чтобы помочь нам понять более широкую картину того, что происходит, и будут приносить дивиденды в дальнейшем в статье и серии, когда мы будем расширять более крупные идеи нашей диссертации.

Я не предсказатель рока. Я не живу в бункере. Я видел слишком много инвесторов, которые падали жертвами чрезмерно медвежьих нарративов, упуская из-за огромной инфляции активов, которую такой негатив запутал. Однако цель этого эссе не состоит в том, чтобы изложить какой-либо тезис о краткосрочных инвестициях. Тем не менее, то, что я начал со все большей ясностью наблюдать как инвестор, как член нашего общества, который заботится о мире, который унаследовали мои дети, все больше свидетельствует о неизбежной ловушке. Ловушка с единственным реалистичным решением. Итак, представленные здесь финансовые данные-это просто инструмент, язык, который поможет нам увидеть это понимание. Фактически, основная идея этой серии гораздо меньше посвящена финансам и рынкам, а гораздо больше-человеческой природе, истории и влиянию стимулов и идеологических конфликтов на исход этого столетия.

Так что терпите меня, пока я веду нас дальше по этой кроличьей норе из обреченных блоков в нашей цепочке реакций.

Блок первый: исторический контекст имеет значение. Оказывается, время-это все

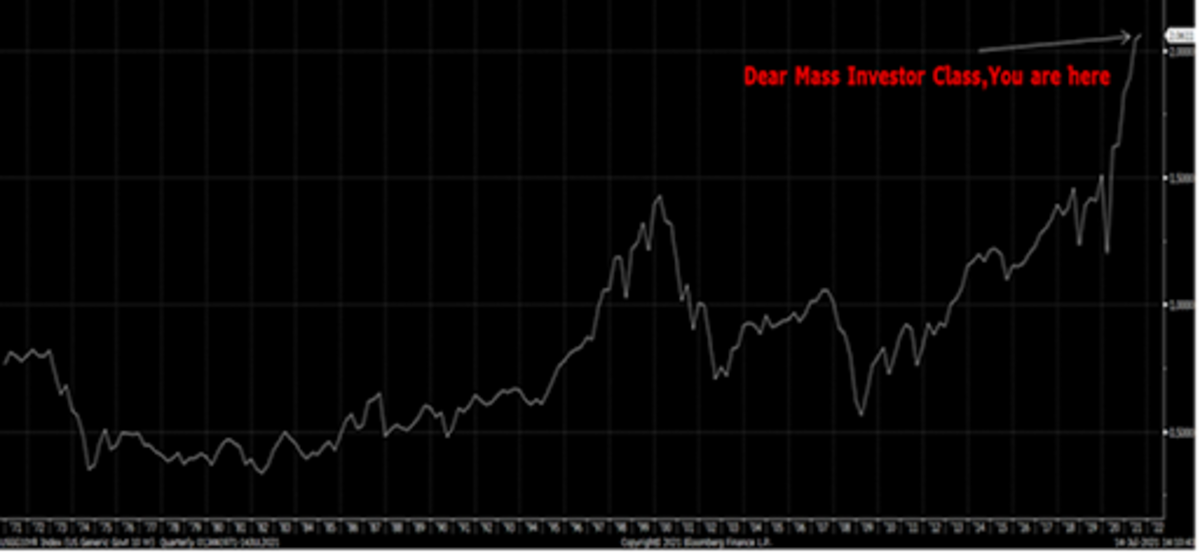

Класс массовых инвесторов, движимый ложными предпосылками и извращенными стимулами, по иронии судьбы формируется после периода беспрецедентной исторической инфляции активов.

Мы только что стали свидетелями беспрецедентных 40 с лишним лет инфляции финансовых активов, накопления долга, дерегулирования и денежного богатства. Эпический бычий рынок облигаций, на котором безрисковая ставка упала с 16% до почти нуля, фондовый рынок относительно нашей производственной мощности находится на рекордном уровне (см. Диаграмму ниже), почти все оценочные показатели находятся на исторических максимумах, а иррациональное поведение имеет резко расширился (примером являются SPAC, r/WallStreetBets, акции мемов, задолженность по розничной марже и, конечно же, многие карманы «криптовалютной» вселенной).

В то же время государственные и корпоративные долговые обязательства также находятся на крайнем уровне. Эти статистические данные становятся еще более чрезмерными, если учесть забалансовые обязательства государства, такие как социальное обеспечение, медицинское обслуживание, пенсионные обязательства и забалансовые оборонные бюджеты. Это в дополнение к учету радужных предположений корпоративного руководства и к тому, что многие команды менеджеров компании отчаянно творчески подходят к уловкам увеличения прибыли и агрессивным стратегиям бухгалтерского учета. Иными словами, индивидуальный инвестор профессионализируется в конце одной из самых больших и самых гомеровских вечеринок за всю историю. Простите за штампованную метафору бейсбола, но это похоже на то, что игрока вызывают из низших лиг прямо перед межсезоньем, после драматического финала Мировой серии с семью играми.

Действительно ли это хорошо для общества? На самом деле это довольно типично для наблюдаемого поведения и участия, которое происходит в пиковые периоды бычьих рынков. Однако здесь есть несколько ключевых отличий от типичного взрыва пузыря.

Во-первых, мы имеем в виду такое поведение в контексте этих инвестиций, которые делаются под видом вновь обретенного профессионализма и расширенных возможностей карьерного роста. Существует чувство права на богатство и ожидания как политиков, так и новых инвесторов, что это их право на получение богатства с помощью рынков капитала, и делать это с очень небольшими вложенными рисками. Кроме того, как свидетельствует снижение уровня участия рабочей силы, общество инвесторов создает двойной риск. Поскольку все больше людей отказываются от других способов труда, мы становимся обществом «арендаторов», а не «деятелей». Мы обращаем вспять историческую стрелу, которая всегда вела к усилению специализации и разделения труда. Таким образом, не только больше людей теперь имеют доступ к финансовым активам, чем когда-либо прежде, но и эта растущая когорта сделала это за счет упущенной выгоды в виде упущенной занятости и полученной заработной платы в других местах.

Ставки выше, а вероятность ошибки ниже. И такое поведение фактически одобряется как в культурном плане, как средство восстания против класса богатых, так и политически, как либеральное право владения активами на большее распределение, независимо от базовой стоимости и риска таких активов. Это отличается от простого временного финансового пузыря. Это воздушный шар, плывущий в стратосфере, чтобы никогда больше не почувствовать твердые объятия земли.

США капитализация фондового рынка по отношению к ВВП в номинальных долларах с 1971 г. по настоящее время. Источник: @LudiMagistR, Bloomberg

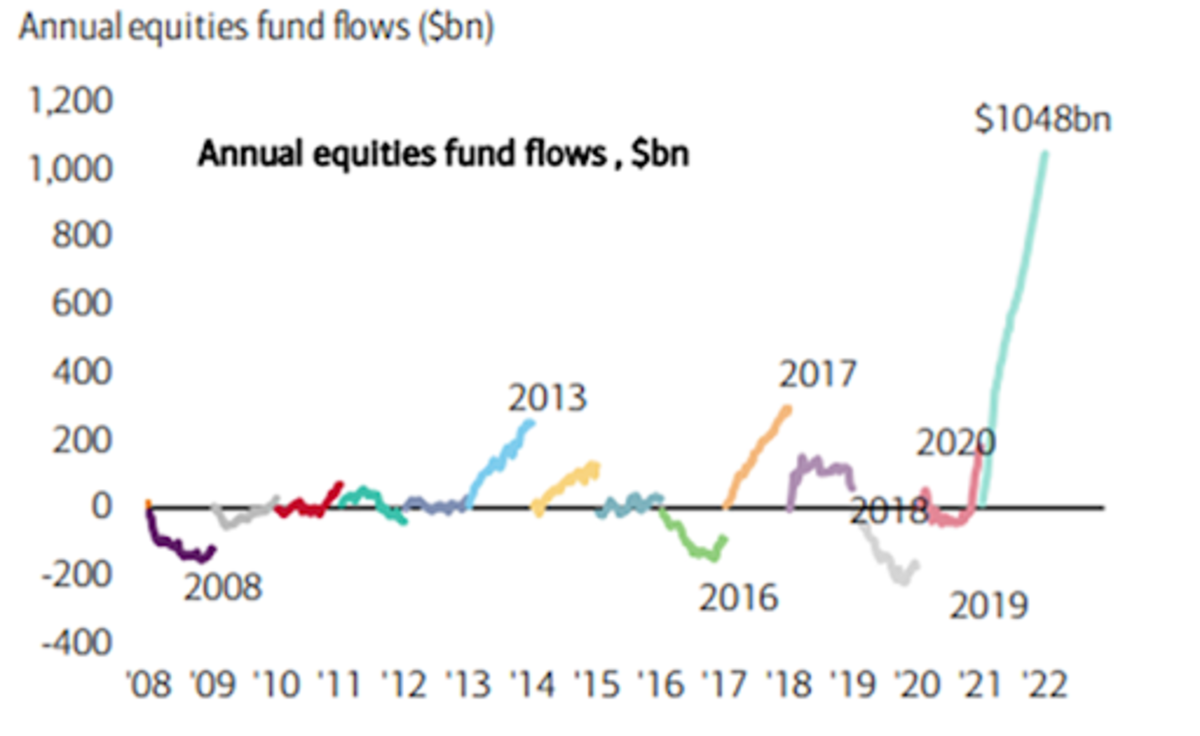

Принятие класса массовых инвесторов ускоряется.

Годовые темпы притока капитала на 2021 год составляют около 1 триллиона долларов. С некоторой точки зрения, это больше, чем общий совокупный приток в акции за последние 20 лет!

Источник: Банк Америки; Майкл Хартнетт

На приведенной выше диаграмме показан годовой приток акций в акции в размере 1 триллиона долларов в 2021 году по сравнению с совокупным притоком капитала в размере 800 миллиардов долларов в период с 2001 по 2020 годы. Подождите минуту, прежде чем продолжить это эссе. В наши дни мы видим так много безумных и беспрецедентных диаграмм, мемов и статистических данных, что этот график легко скрыть. Но это действительно говорит о том, куда движутся дела.

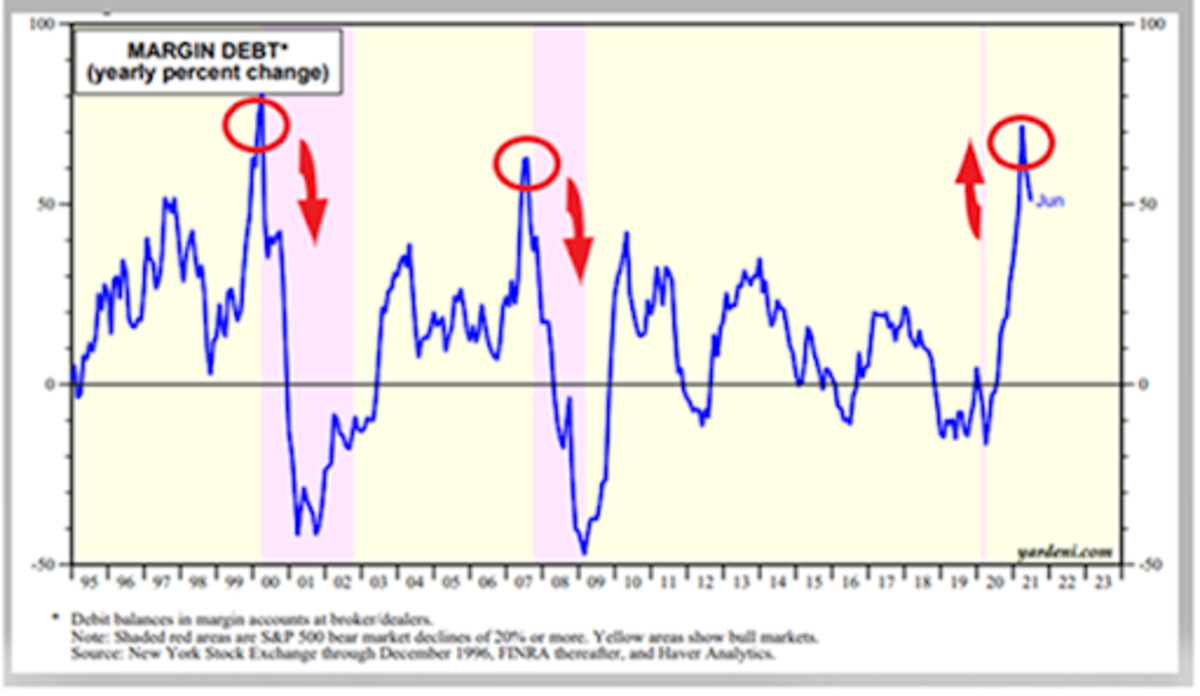

Маржинальный долг для торговли акциями с использованием заемных средств, отслеживаемый Управлением по регулированию финансовой отрасли (FINRA), исторически был признаком энтузиазма и жадности индивидуальных (или «розничных») инвесторов на фондовых рынках.

На приведенной ниже диаграмме показаны ежегодные процентные темпы увеличения маржинального долга, которые исторически предполагали рецессии, отмеченные фиолетовыми заштрихованными областями. Однако мы видим, что в последнее время маржа росла беспрецедентными темпами, возможно, достигнув пика в ближайшем будущем.

Но главное наблюдение здесь заключается в том, что этот быстрый рост произошел после этой пурпурной полосы, а не до нее. Маржинальный долг не предшествовал кризису, а был ответом на него. Мы видели намеки на это в 2009 году, но это было после масштабной очистки банковского и жилищного кредитного плеча, а также значительного списания стоимости активов. Кризис COVID-19 не позволил провести такую чистку и ввел политику, направленную на резкое оживление розничных инвестиций в акционерный капитал. Это новое поведение.

Источник: Эд Ярдени (yardeni.com); NYSE; FINRA; @LudiMagistR

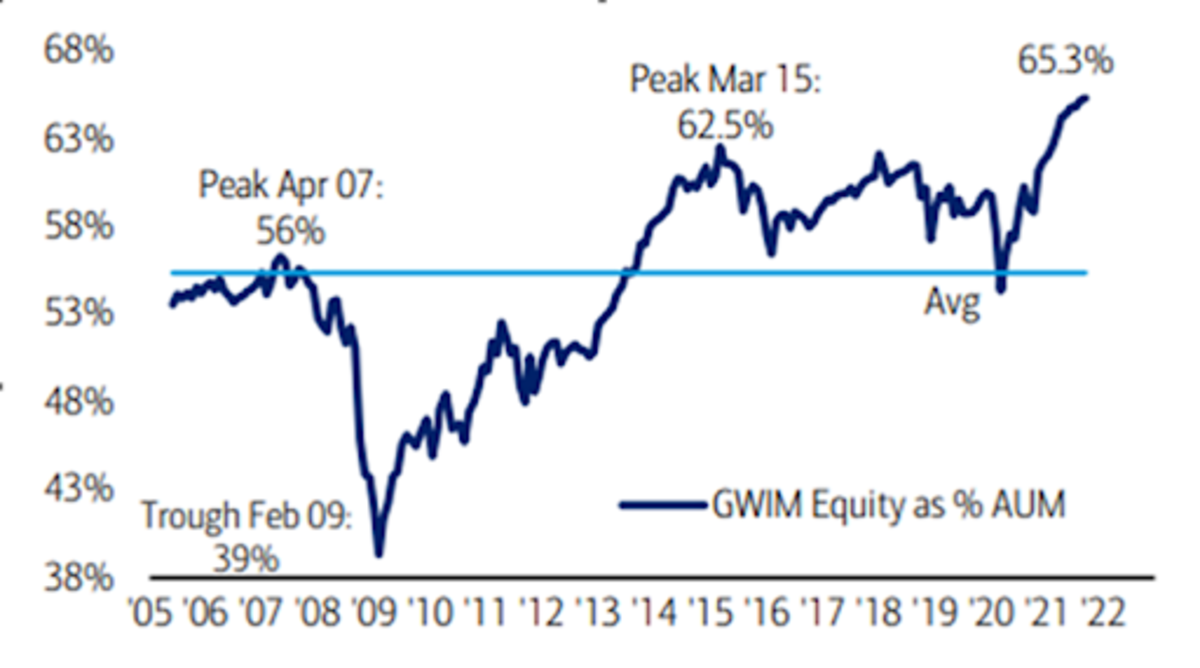

Распределение капитала клиентов Wealth Management Bank of America (BofA) находится на рекордно высоком уровне.

доли частных клиентов BofA в процентах от активов под управлением. Источник: Банк Америки; Майкл Хартнетт

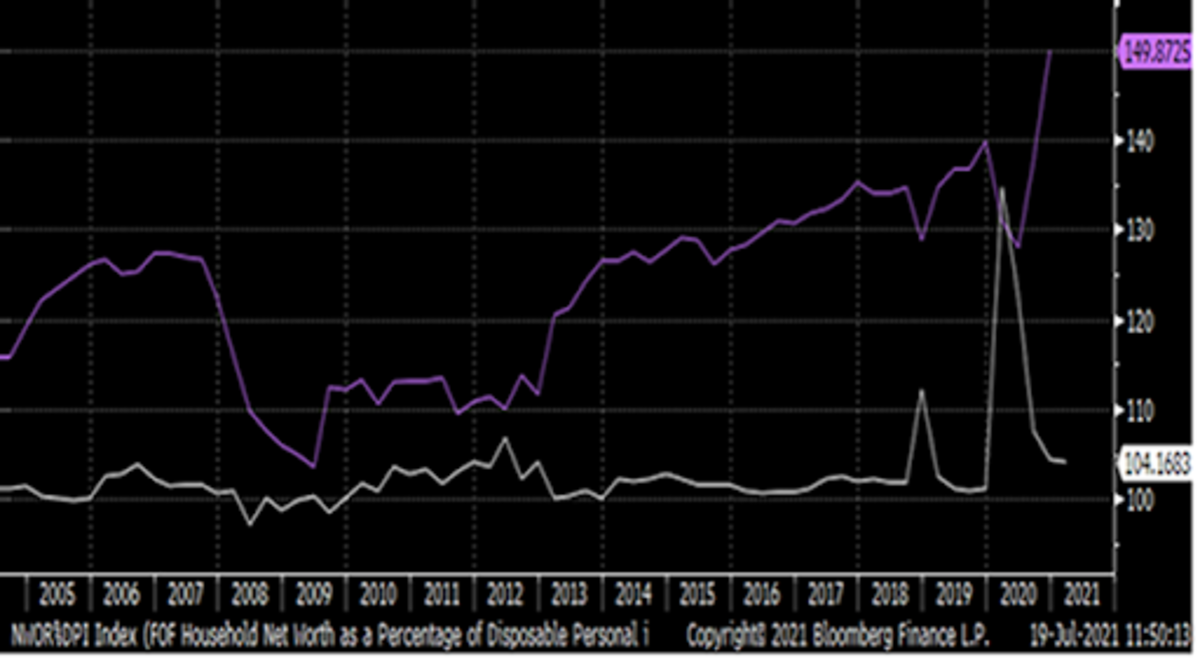

Чистый капитал домохозяйства как процент располагаемого личного дохода (фиолетовый) в сравнении с соотношением темпов роста личных сбережений в годовом исчислении/темпами роста чистого капитала в годовом исчислении (белая линия. Источник: @LudiMagistR, Bloomberg, Федеральная резервная система Сент-Луиса

Последняя диаграмма выше демонстрирует, что люди в США больше накапливают сбережения не за счет избыточного дохода, а за счет инфляции активов. Определенно рискованно а финансовые активы, чувствительные к инфляции, теперь являются основным средством сбережения для большинства домохозяйств, которые могут себе позволить владеть ими.

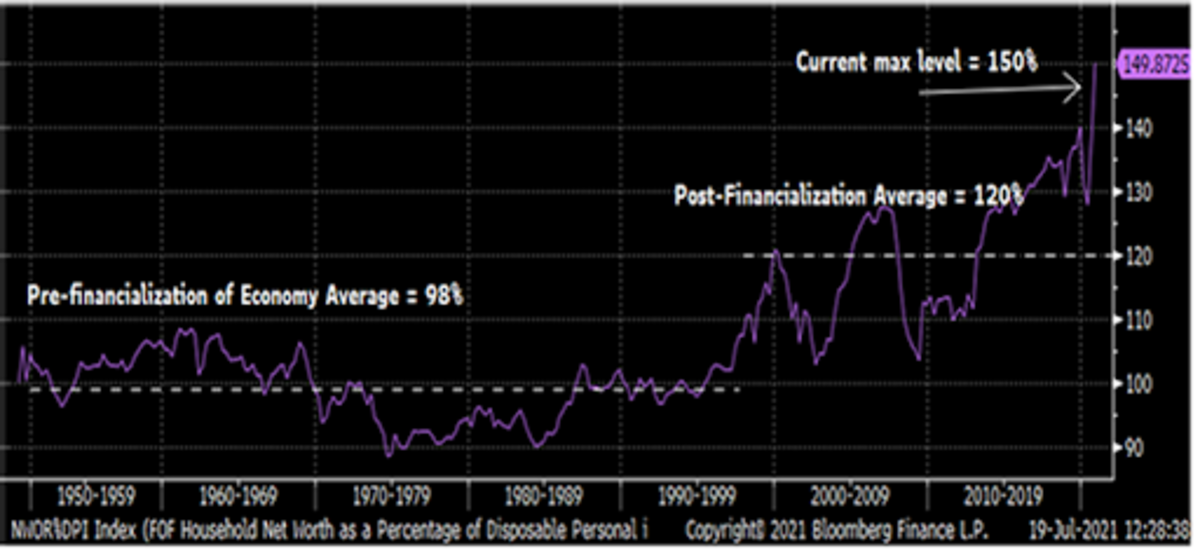

Для более подробного исторического контекста ниже приведен такой же чистый капитал домохозяйства в процентах от располагаемый личный доход, начиная с 1945 года.

Источник: @LudiMagistR, Bloomberg, Федеральный резерв Сент-Луиса

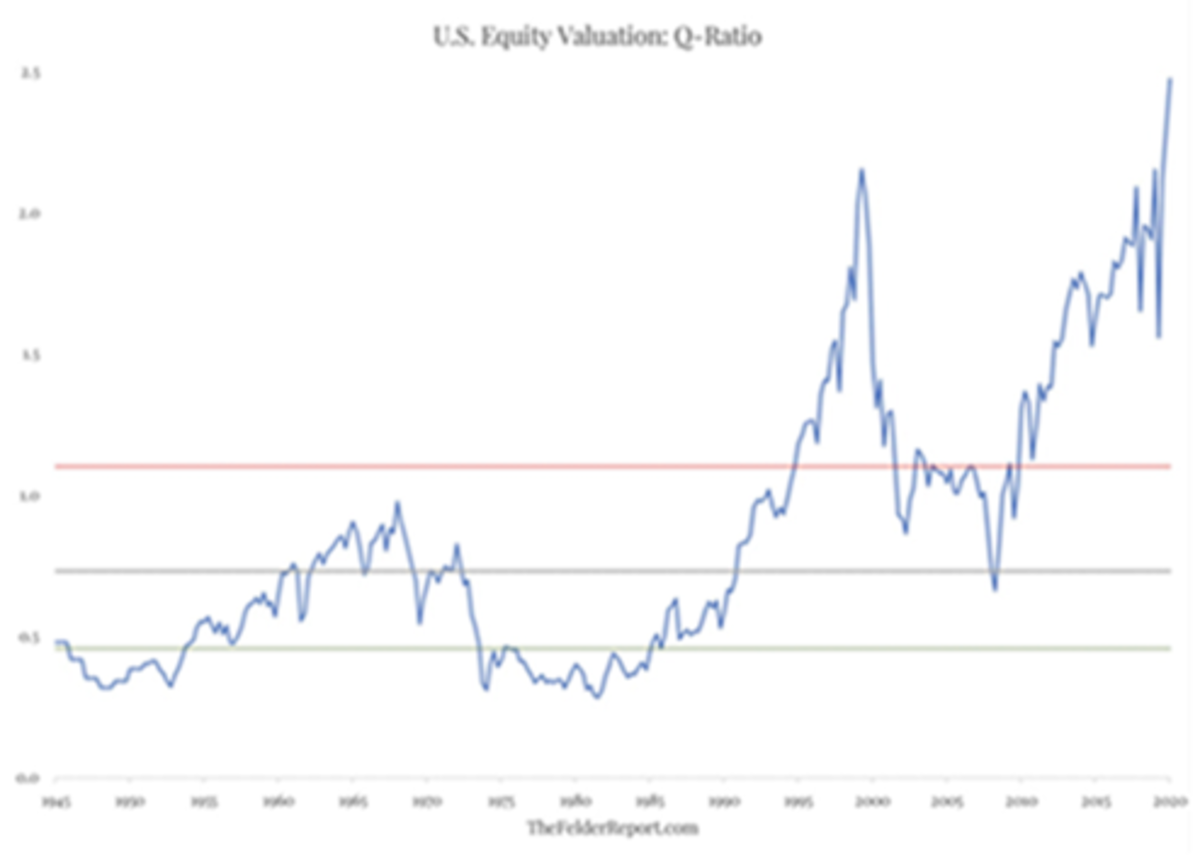

Смерть в случае созидательного разрушения

Ниже приведен график показателя, известного как коэффициент Тобина, также известного как «коэффициент добротности». По сути, это отношение текущей капитализации фондового рынка к реальной восстановительной стоимости активов, связанных с этим капиталом.

Как видно из диаграммы ниже, это соотношение находится на беспрецедентном уровне. График варьируется от периода после Второй мировой войны до настоящего времени и показывает, что стоимость акций в настоящее время почти в два с половиной раза превышает их восстановительную стоимость. Это можно сравнить со средним коэффициентом за 75 лет, близким к восстановительной стоимости.

Следует признать, что этот анализ не лишен нюансов, поскольку наша экономика перешла в информационную эпоху, характеризующуюся в большей степени цифровой экономикой, когда активы становятся более нематериальными и, следовательно, становится сложнее оценивать затраты на замену, такие как интеллектуальная собственность. и доброжелательность сетевых эффектов. Но даже если учесть это изменение, текущее соотношение добротности по-прежнему в три раза превышает восстановительную стоимость по сравнению с эпохой спада 1990-х годов, когда среднее значение восстановительной стоимости составляло 1,4 раза, и post-dot.com. в среднем в эпоху бюста почти в 2,3 раза превышает восстановительную стоимость.

Независимо от того, как вы разрезаете данные, это демонстрирует чистую степень финансовой оценки компаний, полностью оторванных от их экономической реальности. Так называемые «зомби-компании», которые не должны существовать на действительно свободном рынке, часто имеющие большое количество непродуктивных долгов, чтобы поддержать себя, процветают в таком дивном новом мире. Эти сущности улавливают хорошие деньги и держат их в окаменевшем состоянии в разрушающихся структурах. Как профессиональный инвестор, который тратит много времени на инвестирование в высокодоходные корпоративные кредиты, я ежедневно вижу это безумие.

В какой-то момент единственный способ урегулировать такой дисбаланс-это либо массовые реструктуризации, банкротства и дефолты, либо инфляция. Инфляция увеличивает знаменатель замещающей стоимости в алхимическом зелье поверхностной честности. Инфляция, как свидетельствует история человечества, является гораздо более приемлемым решением для экономистов, инвесторов с Уолл-стрит и, конечно же, политиков, которые имеют двух-четырехлетние перспективы развития мира.

Но ирония этого факта в том, что такое осознание должно также объяснить, как мы вообще сюда попали.

Коэффициент Тобина, 1945 г. по настоящее время: оценка фондового рынка относительно восстановительной стоимости экономики. Источник: Отчет Фелдера.

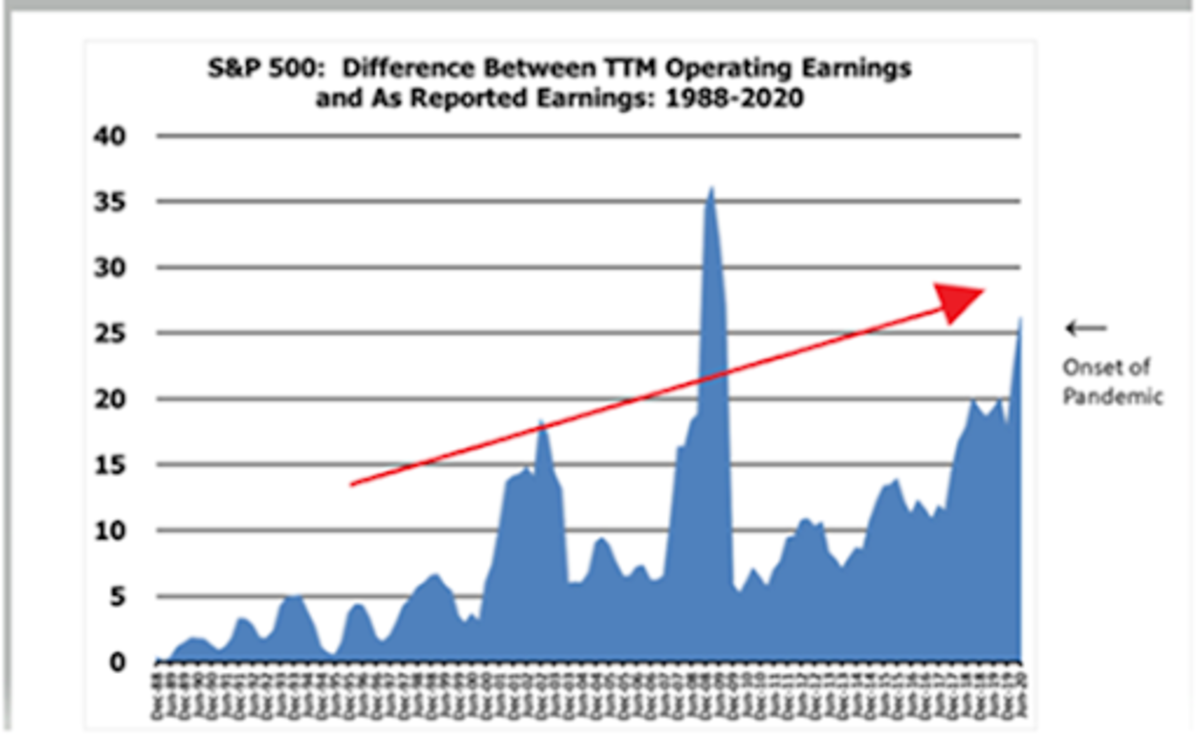

Отрицание качества

Ниже мы можем наблюдать больше доказательств снижения качества. В данном случае мы имеем в виду не только коллапс созидательного разрушения и качество баланса, но и качество самих корпоративных доходов.

Те самые метрики, которым мы доверяем, чтобы помочь нам определить сложный мир данных вокруг нас, были доведены до такой степени, что мера стала целью. GAAP, или «общепринятые принципы бухгалтерского учета», представляет собой протокол бухгалтерского учета, предназначенный для ограничения снижения прибыли посредством непрозрачных, произвольных и вводящих в заблуждение поправок. Иногда действительно существуют действительные корректировки, не относящиеся к GAAP, которые необходимо внести, чтобы получить точное представление об истинном потенциале прибыли компании. В целом, однако, такие «не-GAAP» корректировки отчетности по GAAP, как правило, создают картину более низкой целостности и уверенности.

Несмотря на это, мы настолько привыкли к таким корректировкам, что участники рынка и регулирующие органы не мигая приняли постепенное отклонение. Возможно, неудивительно, что корректировки, не относящиеся к GAAP, впервые стали « неотъемлемой частью финансовой отчетности. »в 1988 году, когда активизировались многие политики финансиализации экономики. Также стоит отметить, что большая часть компенсационных расходов, связанных с акциями, добавляется к прибыли не по GAAP. Таким образом, здесь играет роль самореферентная динамика, поскольку прибыль не по GAAP увеличивает видимость прибыли, помогая завышать оценку акций, что, в свою очередь, приводит к раздуванию самой компенсации, основанной на акциях, которая помогает в первую очередь раздувать прибыль. !

На приведенной ниже диаграмме показан спред между прибылью не по GAAP и прибылью по GAAP:

Этот спред имеет тенденцию к резкому увеличению во время спада по мере накопления внереализационных убытков.. Но что интересно, через годы после рецессии тенденция возобновляет свой путь к более низкому качеству.

Источник: Lark Research

Блок второй: воздушный шар

Результатом этой ситуации является то, что хрупкость системы быстро увеличивается, что требует детерминированной зависимости от пути увеличения объема данных манипулирование, государственная поддержка, регулирование и вмешательство в свободный рынок.

Такой исторический контекст оценки и эффективности активов, как сформулировано выше, означает, что расширение доступа к финансовым активам для более разнообразного и большего населения создает неприемлемый системный риск для экономики в долгосрочной перспективе. Выражаясь словами теории игр, фондовый рынок становится единственной точкой отказа.

Как я изложил в предыдущей статье «Мышление слишком мало и подводные камни инфляционного нарратива», это также становится средством коварной печати денег через создание финансовых активов, а не за счет чего-то большего. очевидное увеличение денежной массы поколений наших родителей, бабушек и дедушек. Этот стимул к раздуванию вследствие морального риска-или неявно гарантированной инфляции финансовых активов-еще проще реализовать, когда технологии делают все больше и больше продуктов и услуг дешевле или полностью обходятся без затрат, а когда ограничения предложения, с которыми мы сталкиваемся сейчас, делают потребление физических «вещей» менее желательны или даже невозможны в некоторых случаях.

Рынки долговых обязательств с надлежащей оценкой создают препятствия для возврата инвестиций, которые стимулируют только те усилия, которые могут создать новый производительный капитал. Чрезмерно дешевый долг стимулирует использование существующего основного капитала без необходимости или желания какой-либо производственной выгоды. И даже когда в конечном итоге производятся новые капитальные вложения, очевидный стимул состоит в том, чтобы сделать это за счет дешевого финансирования, а не за счет сбережений и денежных потоков. Это в конечном итоге приводит к тому, что даже распределители производительного капитала попадают на путь чрезмерного использования заемных средств.

Между тем, когда активы раздуваются, единственный способ поддерживать желаемый уровень жизни заключается в переводе любых сбережений в более рискованные финансовые активы, такие как акции, облигации и т. Д. недвижимость. Это связано с тем, что окупаемость инвестиций для нового накопления капитала всегда занимает больше времени, чем восстановление существующего основного капитала, когда инфляция практически обеспечивается системным моральным риском. Добавьте к этому тот факт, что угнетенные и манипулируемые процентные ставки отбираются из самого будущего, в которое будет инвестирован новый капитал (подробнее об этом ниже). Это еще больше препятствует любым материальным вложениям в новый основной капитал.

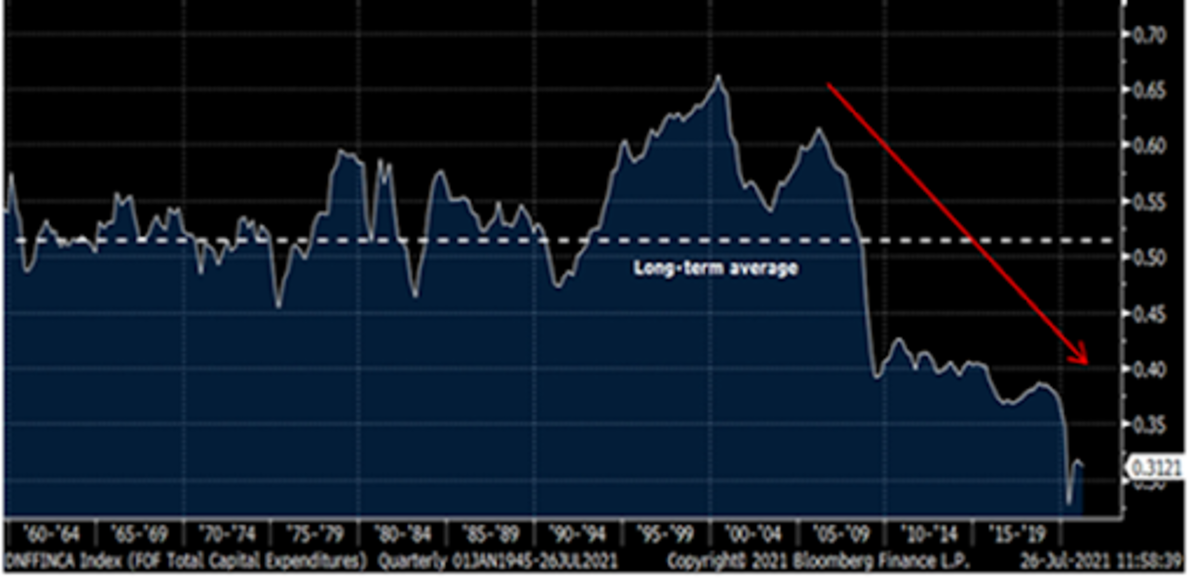

На приведенной ниже диаграмме показано отношение общих капитальных затрат США в номинальных долларах к знаменателю денежной базы, вложенной в систему, измеренной денежной массой M2. С тех пор, как разразился кризис доткомов, инвестиции в формирование нового капитала резко упали по сравнению с созданием новых денег. Возникает риторический вопрос о том, куда текут все избыточные новые деньги, если не в новое накопление капитала. Ответ, конечно же,-финансовые активы.

Источник: Bloomberg; @LudiMagistR

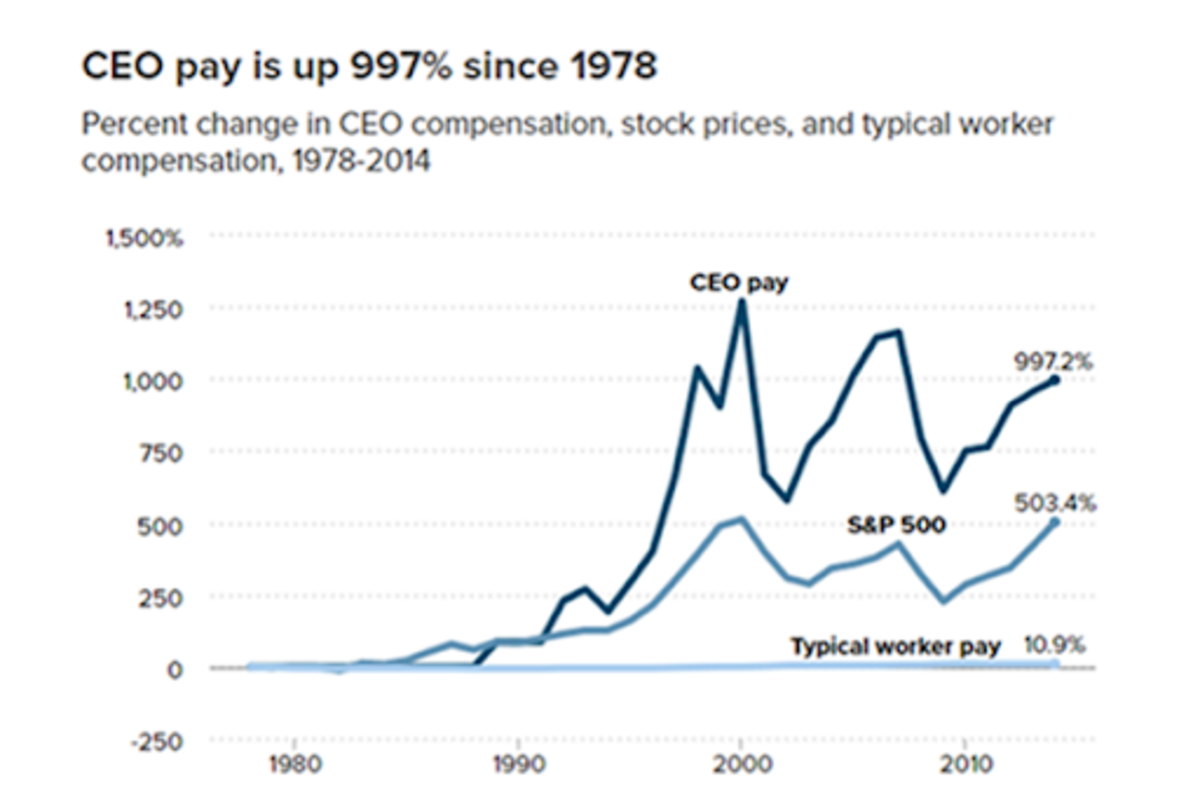

Таким образом, стимулы ясны, как жесткая пуля Столи. И в течение большей части последних 30 лет только богатые были частью этого игрового дизайна, получая место за столом с их существующими активами, их « подтверждение ставки .”

Однако становится все более очевидным, что повсеместный моральный риск, дальнейшее сокращение временных предпочтений и недавно отчеканенные сбережения являются наиболее важными. эффективный следующий этап в этом дереве решений ложной свободы воли. У политиков по обе стороны прохода есть стимулы принять такой нарратив. Они будут стремиться управлять чистым капиталом среднего класса в отличие от старых правил, касающихся повышения доходов среднего класса, образования, систем социальной защиты и перераспределения налогов. Между тем, правая сторона с радостью передаст эстафету от монетаристской экономики со стороны предложения, с ее самообманчивой «надеждой» на то, что американская корпоратократия поделится богатством, а также примет финансовую инфляцию и социализированный капитализм. Правые будут воспринимать такую централизацию рынков капитала как неприятную, но лучше, чем альтернативу кейнсианскому социализму и перераспределению. Обе стороны обменяют свои основные принципы на решение, которое действительно принесет результаты, хотя и с огромной ценой.

Если бы вы были политическим деятелем, глядя на приведенную ниже диаграмму, какой был бы наименее рискованный и наиболее очевидный механизм для устранения такого огромного расхождения? Легко: просто привяжите «обычную зарплату рабочего» к S&P 500-и бум! Миссия выполнена!

Источник: Институт экономической политики; Экономические данные Федеральной резервной системы (FRED)

Хорошо. Итак, давайте предположим, что мы сейчас сдвинулись с мертвой точки и действительно начинаем связывать оплату труда рабочих с фондовым рынком различными способами. Но как совершить такой подвиг? Не то чтобы правительство могло заставить работодателей выплачивать заработную плату в виде фондовых индексов.

Ну, не напрямую. Ответ заключается в смешанном рецепте измененных стимулов. Моральный риск и неявная поддержка цен на акции, как описано выше, безусловно, являются эпицентром такой стратегии.

Но есть бесконечное множество других: увеличение индивидуальных сбережений, вызванное бюджетом, со стимулами для инвестирования любых избыточных сбережений; усилия по деглобализации, которые побуждают граждан США вкладывать больше средств и сбережений внутри страны, а не на потребительский импорт из Китая; и естественное развитие технологий и финансовых инноваций, которые просто «делают свое дело», создавая большие возможности для демократизации инвестирования-примерами этого могут быть такие продукты, как биржевые фонды (ETF), торговые платформы, такие как Робин Гуд, которые упрощают пользователя опыта, блоги в социальных сетях, каналы YouTube и альтернативные информационно-развлекательные платформы, которые укрепляют доверие, а затем окропляют этот бульон изрядной дозой FOMO на культурном уровне. Другим очевидным механизмом может стать повышение налогов на прибыль для направления денег на финансовые инвестиции и повышение налогов на прирост капитала для стимулирования поведения HODLing на фондовом рынке. Это всего лишь примеры. Дело в том, что существует безграничный набор инструментов, доступных для достижения этих целей, как намеренно, так и органически посредством естественных стимулов системы.

«Но подождите,-скажете вы. «Что плохого в более высокой норме сбережений и меньшем потреблении? В конце концов, разве это не основной принцип многих биткойнеров? »

Проблема в том, что даже до такого социального карьерного сдвига, который мы наблюдаем сегодня, уровень цен на активы относительно их фундаментальная ценность уже перешагнула точку невозврата, создав разочаровывающее чувство фатализма у многих непредвзятых участников рынка.

Десятилетия снижения ставок дисконтирования уже украли так много ценностей из будущего, что не осталось даже саженцев будущего, которые могли бы пустить корни. Итак, проблема здесь не в экономии сама по себе, а в конкретных сберегательных пастбищах, на которые пасутся люди. Экономия не является экономией, если она не направляется в реальные средства сбережения. На самом деле как раз наоборот. Единственный способ поддерживать текущий уровень жизни требует постоянных темпов роста цен на активы, что, в свою очередь, приводит к увеличению долга.

Если бы правительство и нормативные культурные влиятельные лица экспортировали такую динамику в массы, какого результата мы должны ожидать? Утопическое равенство и изобилие? Или это централизованное планирование, маргинализированный свободный рынок и социализированная экономическая деятельность? Ты угадал! Дверь номер два, Боб!

Источник: Business Insider, CBS

Блок третий: математика

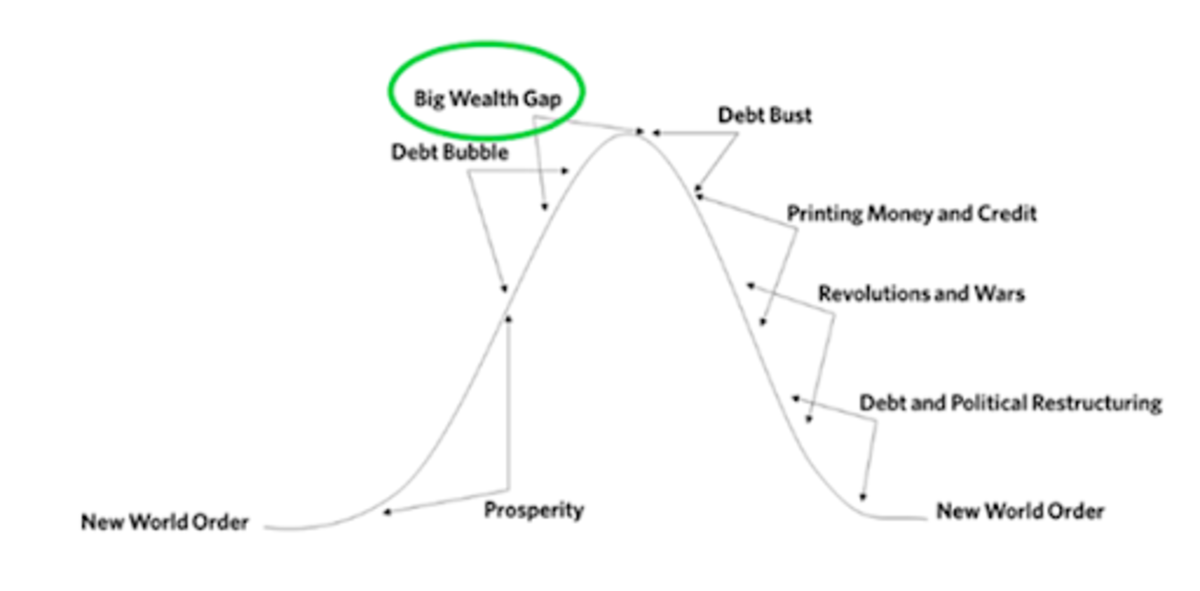

Одна из самых влиятельных переменных, которая исторически ассоциировалась с окончанием периодов большой стабильности и силы. было неравенство богатства. Хотя такая асимметрия редко является причиной системного коллапса, она почти всегда является симптомом распада и столь же часто играет роль в катализировании переломного момента в упадок. От майя до Римской империи и трех китайских королевств, османов и французской, русской и китайской революций неравенство богатства всегда играло важную роль.

Источник: Рэй Далио,« Меняющийся мировой порядок », первая глава

Это большая проблема для стратегии массового инвестора. This is because a goal of wealth redistribution with a strategy centered around asset inflation is statistically impossible to achieve.

Many proponents of this new investor class take the “fight fire with fire” approach. Yes, asset inflation — driven by modern monetary policy — has been the prevailing impulse of inequality over the last several decades. Why should the average individual not be able to get their just desserts as well? Ethically speaking, I take no issue with such retribution to some degree.

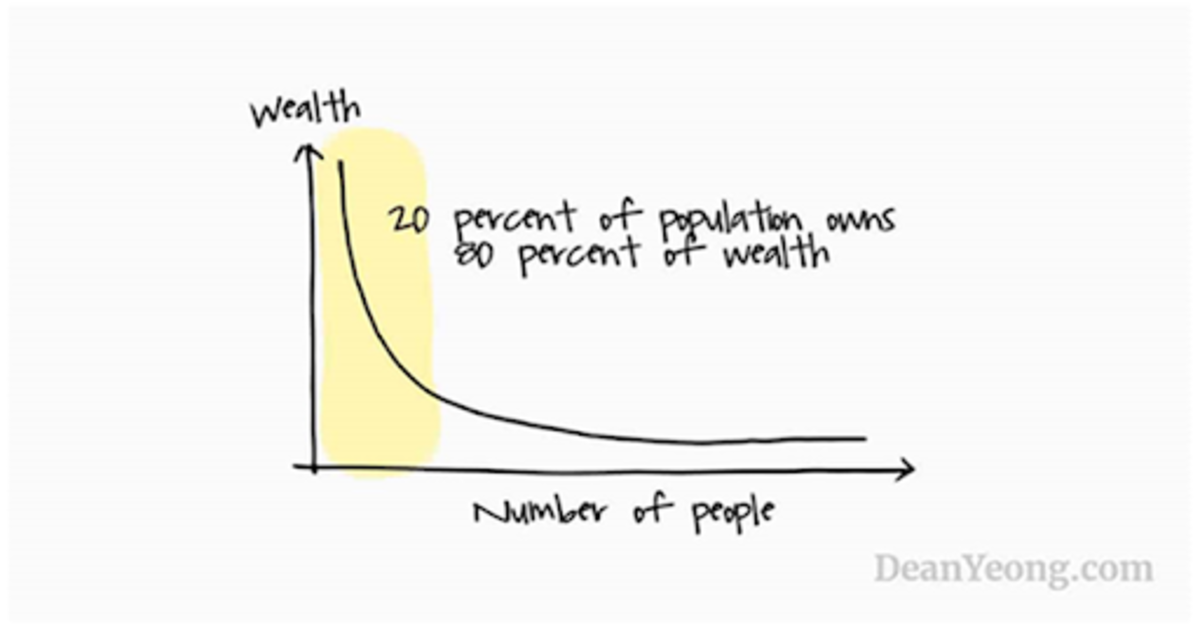

Unfortunately, it’s an illusion. The presiding growth curve that has been empirically witnessed as it pertains to wealth distribution has been found in the Pareto principle, a probability distribution whereby a small percentage of the sample group acquires most of the attainable value. Facets of this law, more colloquially known as the “80/20 rule,” are observed not just in wealth distribution, but prolifically throughout much of nature and human social environments.

We have experienced at least a half-century of Cantillon effects that have supported asset owners in exponentially outperforming relative to income owners. Even if we disposed entirely of such Cantillon effects and allowed the broader population equal access to financial assets going forward, and even if financial assets continued to generate historically anomalous returns, the “80 percenters” would never catch up. The reason for this is simply due to the nature of exponential growth curves as seen in the Pareto principle. Inequality would be maintained at the very least, if not continue its asymptotic expansion.

Pareto’s law: How asset inflation becomes a highly entropic state for wealth distribution, regardless of policy.

Source: DeanYeong.com

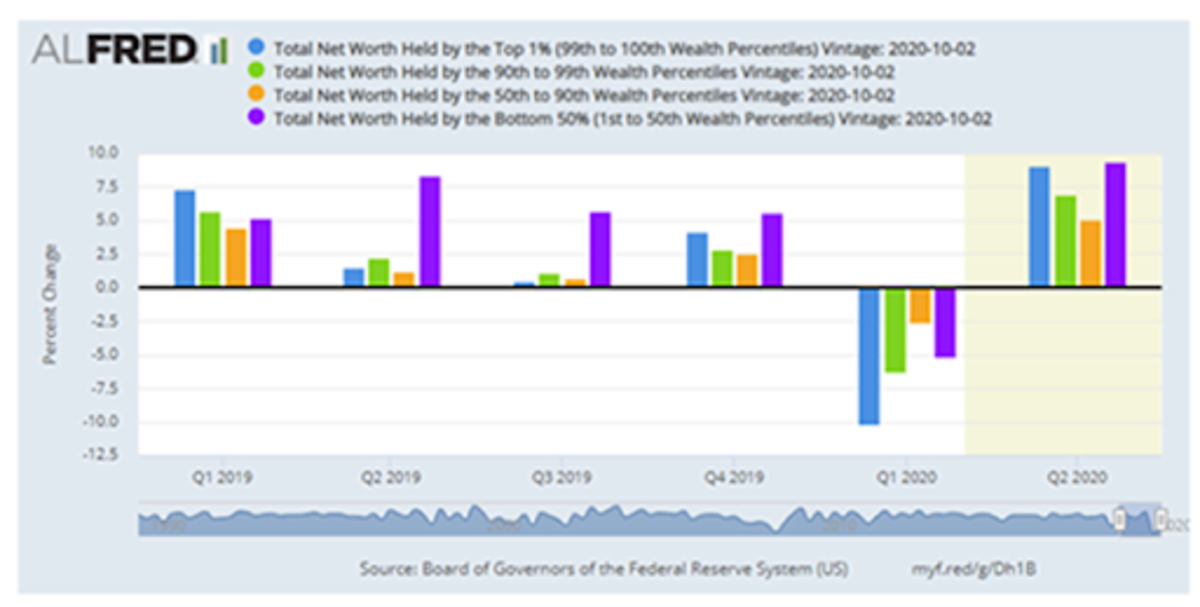

This Pareto probability distribution is exemplified quite dramatically after looking at 2020 as an outlier year, whereby the least wealthy percentiles actually saw the largest percentage improvement in wealth. However, while this is a lovely-sounding statistic for social media hype and political propaganda, it is purely a mathematical outlier caused by starting from such a low base and from such a low level of prior financial asset ownership.

Unfortunately, the banner year for the bottom 50% (purple bar below), did next to nothing to narrow the wealth gap from the top percentiles, as evidenced by the below chart.

Source: Federal Reserve

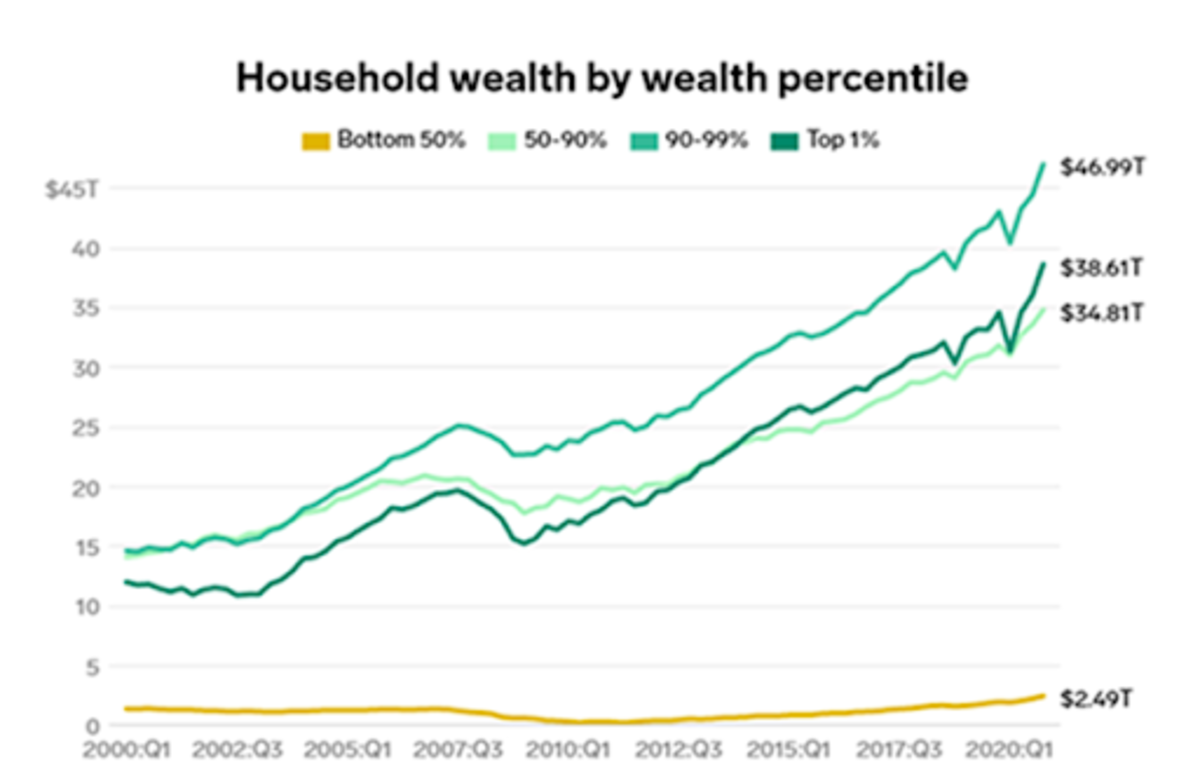

2020 did nothing to rectify the problems of inequality. In fact, inequality only got worse. Why would a continuation of asset inflation look any different in the future?

Source: Federal Reserve, “Distributional Financial Accounts”

If inequality cannot be corrected by the only policy tools available, the risks for social instability will only rise further. Ironically, when stability is threatened, this tends to only increase levels of centralization.

Have you ever been driving your car on a wet, slippery road, only to fish-tale unexpectedly? While our instinctual response would be to tense up and violently steer the wheel in the opposite direction to regain control, such a reaction would only worsen our dire predicament. One must steer into the chaos. Once control has gone, such a fate must be embraced, not opposed. This is the only way out. Further attempts at control only make matters worse.

Block Four: All Roads Lead To One Road, More Centralization

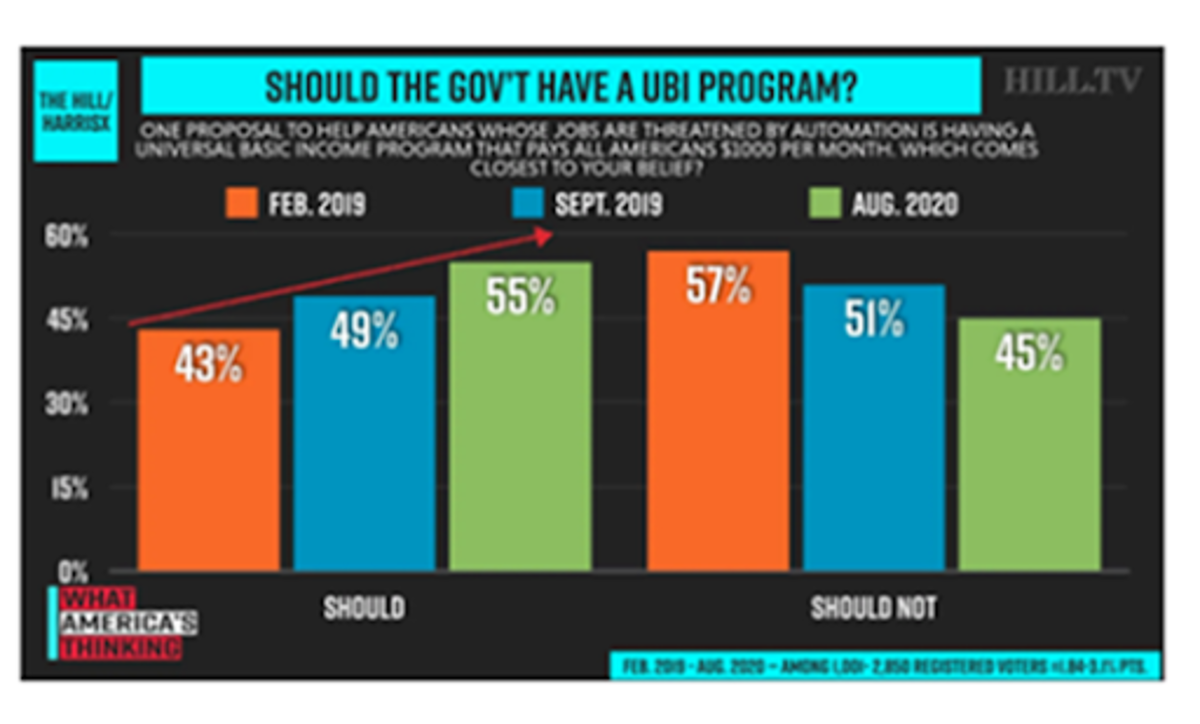

Once the inevitability of blocks one, two and three as stated above are appreciated, the path dependency of block four in our chain becomes absurdly apparent: Subsidizing asset prices through monetary debasement becomes the oblique way that society yields to ideologies like universal basic income (UBI).

UBI may end up in the very long run as explicit social welfare programs, or “helicopter money.” Of course, during COVID-19, we saw some discreet examples of this, turning something merely theoretical into a tangible part of the societal zeitgeist. However, it is a mistake to assume a linear path, that such policy will now settle as the initial and most effective vector for such policy going forward.

A more frictionless pathway would be the mechanism outlined above, whereby social welfare can be extolled circuitously. The brilliance of such a policy approach is that it would not require any incremental pieces of legislation, and no constitutional alterations to property rights. There are no foundational legal constraints. This implies that our current institutions have the power to accomplish such social welfare goals today.

One could argue that some changes would certainly make these aims easier to administer, like augmenting the Federal Reserve Act of 1913 and expanding the powers of the U.S. Treasury Department. However, the key point here is that such change is not required. If the reader finds this too far fetched, I would recommend listening to the taped conversations between ex-President Richard Nixon, and then-Federal Reserve Chairman Arthur Burns. It has happened before in this country, and in less dire circumstances.

Source: TheHill.com

UBI advocates are here, and they have their own network effects:

“The map references not only networks with the sole purpose of advocating UBI, but also all organizations (networks, foundations, platforms, political parties, working groups within political parties, societies, study groups, etc.) that advocate for UBI.” Source.

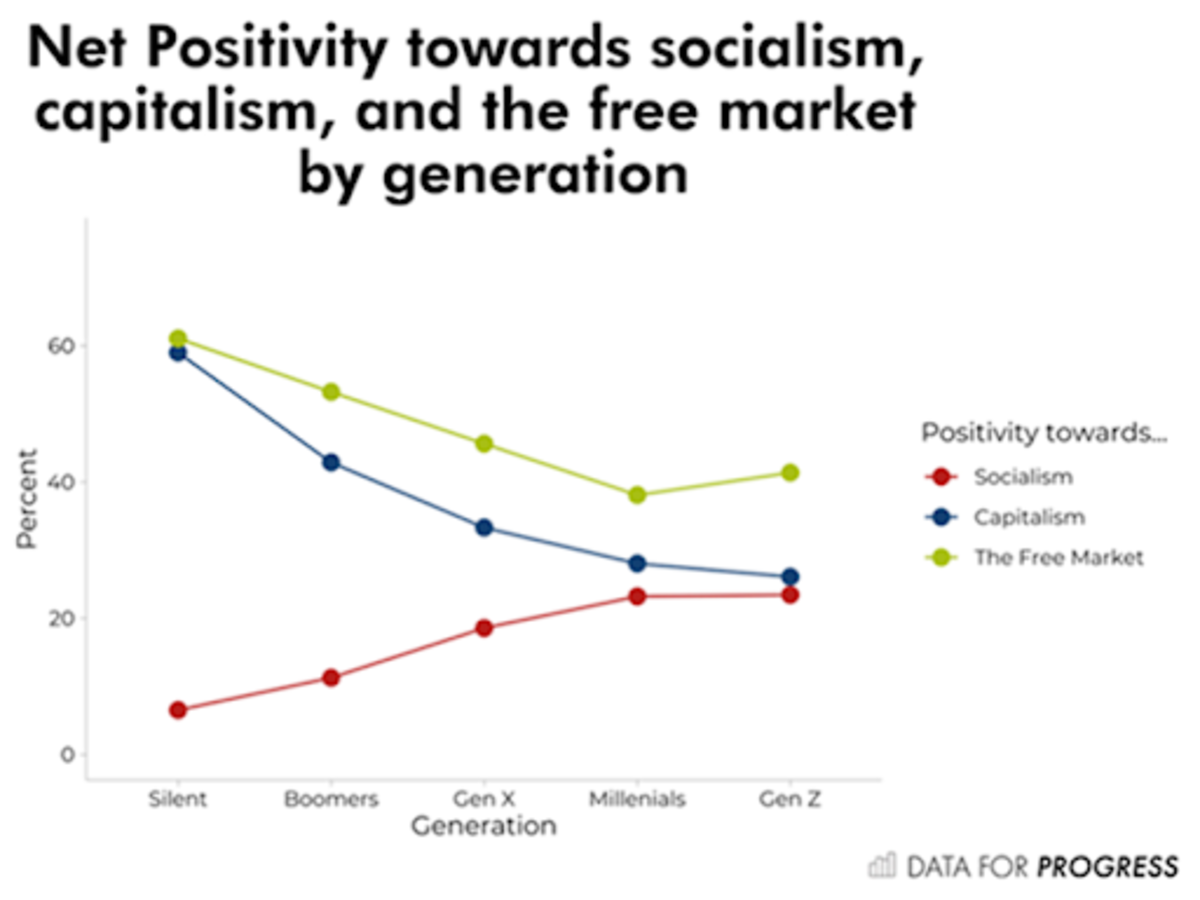

American openness toward socialism, and a commensurate disdain for capitalist ideals, has increased dramatically over the last four generations. This has been well documented with recent generations, particularly millennials, but it is important to recall that such a trend has been consistent well before that, even with the boomer generation relative to their parents and grandparents.

This is rather alarming when one considers that this generation has been the biggest beneficiary of financial asset prices (coincident with the full embrace of the fiat monetary system) of any generation in American history.

A Quick, “Passifict” Detour: Passive Investing Socializes Capitalism

Bitcoin may be humanity’s historically most perfect manifestation of a pacifist revolution, but passive investing is also a revolution, only with completely opposite implications.

Historical analogues are always dangerous, and each generational crossroads exhibit unique characteristics that can change the entire spectrum of outcomes. However, as a reference point, current trends reverberate with echoes of previous centralizing efforts designed to redirect our collective future and shift the public behavior, reminiscent of Franklin D. Roosevelt’s “new deal,” as well as Nixon’s “great society,” or even going back to German Chancellor Bismarck and his social welfare policies in the 1880s, which greatly enhanced the Second Reich’s military capacity.

Passive or indexed investing vehicles such as exchange-traded funds (ETFs) are yet another example of this shift toward a “mass investor class.” While such a trend may seem innocuous, it is cultivating the seeds of enormous societal change.

As discussed by Inigo Fraser-Jenkins, a highly-regarded maverick quantitative equity strategist at Wall Street firm Bernstein, passive investing can be compared to Marxism. This may sound hyperbolic, but unfortunately, I believe he is on to something important here, the point being that the democratization of capital markets by way of ETF proliferation and other passive investing products inadvertently leads to a socialization of capital.

It would all but complete our societal transgression from liberal democracy to social democracy, a trend that has been gradually underway, but accelerating over the past 75 years. Fraser-Jenkins compared passive investing to other societal externalities like the tragedy of the commons, whereby behavior that may be optimal for the individual investor can be quite negative for the aggregate society when all actors behave the same way (we will return to the problem of the commons later).

The unfettered expansion of passive investing does not look likely to subside any time soon. This is especially obvious when one simply looks at the below chart, or even at the hiring behavior on Capitol Hill, like the large representation of Blackrock alumni acquiring key roles in the current White House administration. Blackrock is the number-one manufacturer of passive investment vehicles in the world, with over $1.8 trillion in assets under management (followed by Vanguard in second place at $1.2 trillion).

Additionally, ESG and clean energy investment mandates further this shift, creating new products to bundle into thematic passive investment securities. Such bundles make it easier for ESG-approved companies to redirect capital away from those companies that do not fit the homogenous definitions prescribed. To be clear, there is nothing intrinsically bad about incentivizing cleaner energy and more sustainable economic practices. Of course, this is a good thing! However, when rules for such behavior become formalized, complex, and sometimes arbitrary and naively general, they impinge upon the competitive dynamics of free markets that would accomplish such goals more effectively.

Instead, such rules generalize the flow of investment, compensating those market participants best suited to game such a system. The new game defines the winners as those best able to adhere to the appropriate definitions as a means of acquiring low-cost capital. In a road paved with good intentions, we potentially end up in hell, robbing free markets of innovation, nuance, and differentiation. We write new rules of the game, rules that thoughtlessly increase centralization.

Mike Green, a distinguished researcher of passive investment stated back in 2020:

“Of managed assets, [passive investment] is now greater than 50% [and over 40% of total market capitalization]. That split though, is not uniform across demographics. Millennials are almost 95% passive. Boomers are only 20% passive. For the vast majority of millennials, their only exposure to the market… We make a lot of hype about things like Robin Hood and stuff, but the actual assets are tiny. The vast majority of the money that they’re getting is actually just going into things like Vanguard target-date funds.”

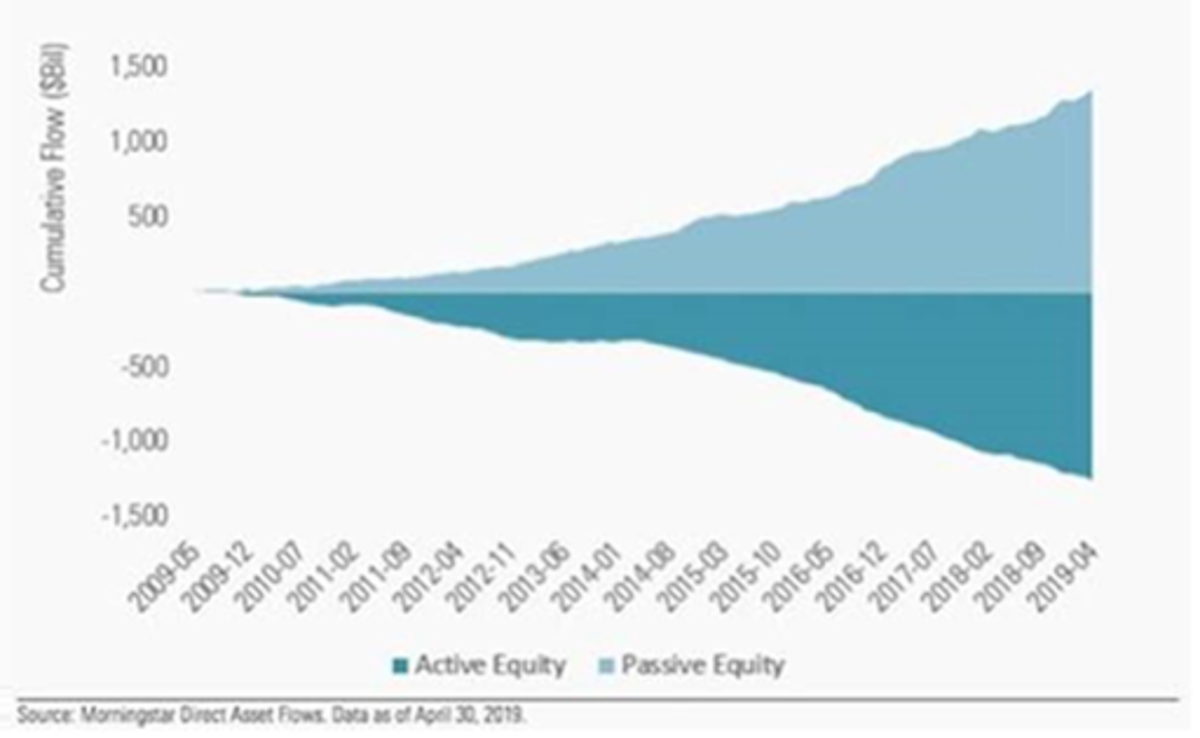

Active equity managers have seen outflows every year and passive investment vehicles have seen inflows every single year since 2006. And this trend is only accelerating:

Source: Morningstar

Source: The Wall Street Journal

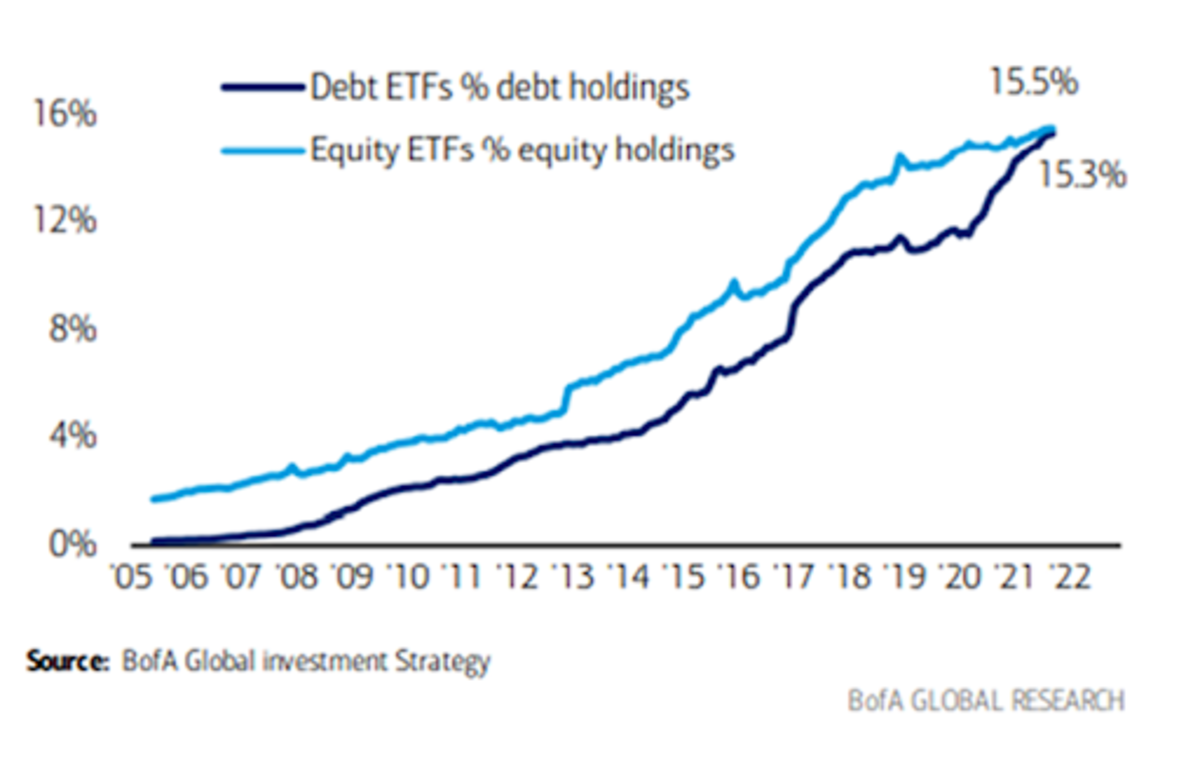

Bank of America’s private client ETF holdings as percentage of assets under management (AUM). A hard trend to fight:

Source: Bank of America, Michael Hartnett

The passive singularity: Millennials have 95% of their retirement savings invested in passive vehicles. What is the logical conclusion of this freight train?

“One of the challenges that gets created as passive becomes a larger and larger share is that there becomes no discretion. There is no consideration of should the incremental dollar go in in the exact same fashion, right? That passive player has no instruction to sell. You exhibit increased inelasticity in terms of each incremental dollar that goes in. Imagine a scenario in which 100% of the owners of a company were passive and you tried to buy a share. There is no price at which they would be willing to sell to you unless they received an instruction from their end investors saying to sell shares to you. Prices could theoretically become infinite on that type of dynamic. Eventually, you would expect somebody to respond by saying, ‘All right, I will sell an additional share to you.’ Traditionally, that’s been accomplished by price-sensitive or return-sensitive discretionary managers who say, “Okay, this price is unwarranted by the fundamentals. Therefore, I’m willing to sell some of these shares to this person who’s expressing, in my view, an irrational demand for these shares.” If that demand is so strong and it gets absolutely extreme, people can synthetically create shares by shorting, but that is incredibly dangerous to do, an environment in which stocks are exhibiting this reduced elasticity.” –Green

The mass investor class faces a big incentive problem: What does the internet, digital property, and a tragedy of the commons have in common? Our retirement accounts.

The dismantled connection of choice from the capital allocation process brought about by passive investment proliferation has implications beyond the clear destruction of price signals. This is no small statement. A destruction of price signaling is as destructive as things can get for a capitalist system. Prices are the main form of communication we use in society to make appropriate economic decisions and choices. Its dissolution is of existential importance.

However, there are other problems to consider from this evolution of behavior as well. Ever since the runup to the 2016 U.S. presidential election, and at an accelerating pace since the onset of the COVID-19 pandemic, society has become more aware of the vast concentration of power that the internet giants and social media platforms carry.

Pockets of government and pockets of new and growing cultural progressive movements have quite easily influenced and incentivized these platforms to actively censor speech in our democracy. This is not a political statement, and this is not a judgement about the people being censored, but merely a factual observation about a key tenant of our democratic institutions. If the U.S. Constitution can be likened to the “core protocol algorithm” dictating the manner in which our collective network operates, this is a clear attack on one of the most vital rules of the protocol. How can we so readily dilute our core principals?

First, network effects are powerful. The ability of the internet companies to sustain and grow off individual resources, with extremely low detachment rates, cannot be underestimated.

How did this come to be? A failure in timing. As is often the case with disruptive technology, its usage preceded an appropriate infrastructure to handle it. Unfortunately, the Byzantine Generals Problem was not solved before the advent of the internet. Consequently, we have been suffering the consequences that a lack of enforceable property rights leads to in a digital world. A winner takes all society.

This is what the internet got wrong. You didn’t own anything. No one had any stake on the internet. Instead, value has been extracted by those who figured out ways to own the on-ramps and access points to the internet instead.

This group has become the “landlord class” of the internet, and the vast majority of value proffered by the internet and its myriad innovations of social communication has been funneled through this layer. The consequence, of course, has been more inequality, more surveillance and control, and more concentration of power. Further, we’ve witnessed a trend toward a reduction of quality of information. There is a diffusion of responsibility that engulfs the internet when ownership is so opaque and ephemeral. We are incentivized to create more noise than signal because when no one owns the land, there is no incentive to be a steward of that land to ensure its long-term sustainability, utility and productivity. Instead, the incentives align so as to be solely transactional. The more information one can manage, control and recapitulate, the more one can develop network effects and externalize the social and economic cost of a system that produces excessive noise and underproduces enough structured signals that could offer synergistic benefits across societal planes. That cost is shared by all of society. It’s a tragedy of the commons. All because the internet couldn’t address digital property rights.

The second issue here is that network effects also impact passive investing. Most passive vehicles are ETFs, that are indexed and weighted by market capitalization. The bigger you are, the more capital you attract. Size matters, aptitude and productivity do not. This takes us back to the Pareto principle and the 80/20 rule, setting the stage for increasingly non-linear distributions of capital. And in a world where access to low-cost capital is a massive competitive advantage, we end up with an obvious outcome. The big continually get bigger, and the small get only smaller. Or worse, the upstart disruptors may never have a chance, and we would never even know what could have been.

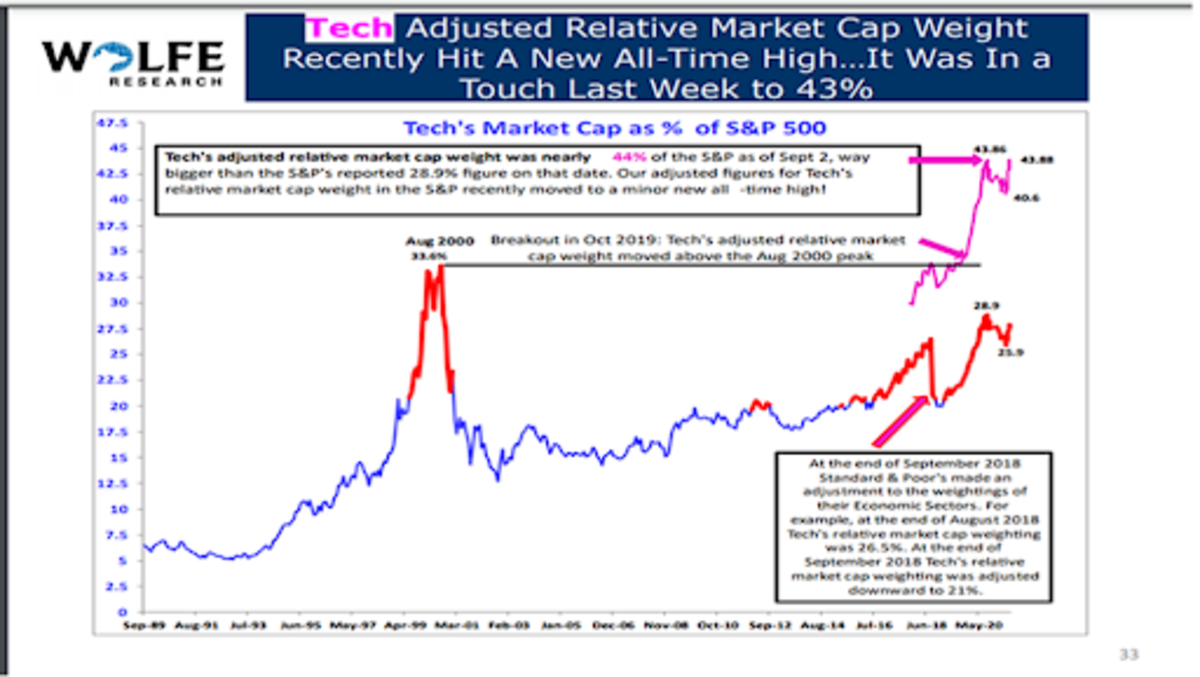

That brings us to the present, where just six behemoths have a near majority control of the entire equity market. Most investors do not blink at this statistic any longer. Professional investors have been numbed to such lopsidedness. However, imagine if such inequality persisted within the domain of political parties? In democratic institutions? In your childrens’ classrooms? But the real question we need to start seriously and honestly asking ourselves is this:

If the below chart only becomes even more extreme in its weighting distribution, and if our collective wealth is increasingly tied to the index it represents, what will our incentives be as the companies involved become even more centralized?

About 45% to 50% of our savings are tied to companies that could be actively censoring us, and indirectly eroding the very principles of the system that allowed them to prosper. This share of our savings will only grow further. Will we object? Я очень на это надеюсь. But so far, there is little evidence to support that aspiration. Unfortunately, passive investing, alongside a mass investor class, is likely to only help internet platforms and capital markets centralize further.

Major stock indices are mainly just six names now: Apple, Amazon, Facebook, Google, Microsoft and Nvidia, totaling 42% of the equity market.

Source: Wolfe Research

Block Five: All Roads Lead To Zero

What happens when zero volatility is the new equilibrium?

After our modest digression into passive investing, let us now return to the last block in our chain. The final and most deadly flaw in the chain reaction socializing financial assets relates to volatility and the cost of capital. Mathematically speaking, publicly-administered financial markets that demand continuous appreciation, distributed broadly and without diversification, will require volatility to trend toward zero over time.

A simple law in financial markets, when assessing an asset’s volatility (as measured by its standard deviation of returns over a given period), is that the more vulnerable to uncertainty an asset is, the less it can absorb volatility. This is why, for example, equity investors are generally willing to pay lower valuation multiples for cyclical or economically-sensitive sectors relative to secular growth or defensive industries. These types of companies are more vulnerable to unforeseen events. When our financial markets are a tool of policy rather than an expression of free market capital allocation, we eventually become incapable of withstanding any uncertainty. And manipulation to affect policy outcomes would be the only way to ensure uncertainty’s suppression. If successfully orchestrated, volatility must eventually collapse toward a zero bound to accommodate this.

As our centralized debt trap expands in circumference, the risk-free rate must also trend toward zero, as has been the case over the past 40 years. Over time, the consequence of this could even be the elimination of the need for a private sector.

This last section is essential to our thesis, as it is the bridge that transports us from the current transitional sandwich era where we find ourselves juxtaposed between centralization and decentralization. This is the last stop on this transitional train as we push relentlessly down the path toward a more authoritarian world order. Given its level of importance in our story, it requires some more detailed explanation.

Centralization As A Black Hole: The Volatility Singularity

Source: Disney, Pixar

What is the volatility singularity? Previously, we have established the logical chain of cascading events that are required in our world’s existing model.

Debt must go up, so stocks must go up. Thus, rates must go down, so volatility must go down. When this happens debt will logically go up, leveraging the system even more, so stocks must go up to prevent collapse and inflate the debt bubble with a greater equity cushion… (stop for breath)… So, rates must go down again until zero, so volatility must go down until zero.

Volatility collides with zero. Everything goes to infinity. Yippie! The transcendent state where the difference between nothing and everything gets very fuzzy and rather philosophically confusing. Just as observed in the case of black holes, where physics starts to behave mysteriously and spooky as one approaches the event horizon, so too do economies. Things start to get pretty eerie as we approach the zero point event horizon in volatility.

Thinking about the problem in the following simplified manner may be helpful:

Anything divided by zero equals infinity. Financial assets returns are a function of volatility. A common formula used to calculate risk-adjusted returns is called the Sharpe ratio, which is an asset’s return during a given period, minus a market risk-free rate, divided by the investment’s standard deviation of returns. If volatility is, for all intents and purposes, equal to zero, so too is its standard deviation. Thus, we end up in a confounding situation in which excess returns are divided by nothing, and therefore magically become, well… everything.

Image source. Source of quote: Kurt Vonnegut, “Slaughterhouse-Five”

As macro volatility fund manager Christopher Cole excellently laid out in a 2020 piece titled “The Allegory Of the Hawk And The Serpent,” an investment strategy designed to short volatility, or benefit when it decreases, experienced temporally anomalous returns since the early 1980s, right when the financialization of Wall Street took off exponentially, and right as Alan Greenspan et al. began a campaign of moral hazard, at a time known as “The Greenspan Put.”

The stock market and nearly all financial assets in aggregate then become just a mere proxy for this “short volatility” expression.

Source: Artemis Capital, @vol_christopher

An Endangered Golden Goose

Cole, like many others, believes this period of declining volatility is mean reverting and must therefore repeal its nearly 40-year journey. While certainly possible over a cyclical short term time horizon given the magnitude of the move, a spike in volatility is unlikely to be palatable for any sustained period. The reason, as you might have guessed, is because of the deterministic nature of acceptable outcomes laid out above. The violence to the system that a spike in volatility would require would eviscerate so much wealth, so many debt obligations, that the policy response would be equally violent. Such a response is all but guaranteed because the crisis would be existential for those in power.

This outcome becomes more assured each day that goes by with greater reliance on financial assets to lift us into the future, each day that a citizen puts their first dollar of savings into such a system, and each day that another dollar is diverted away from new capital expenditure in favor of being recycled instead back into the existing sinkhole.

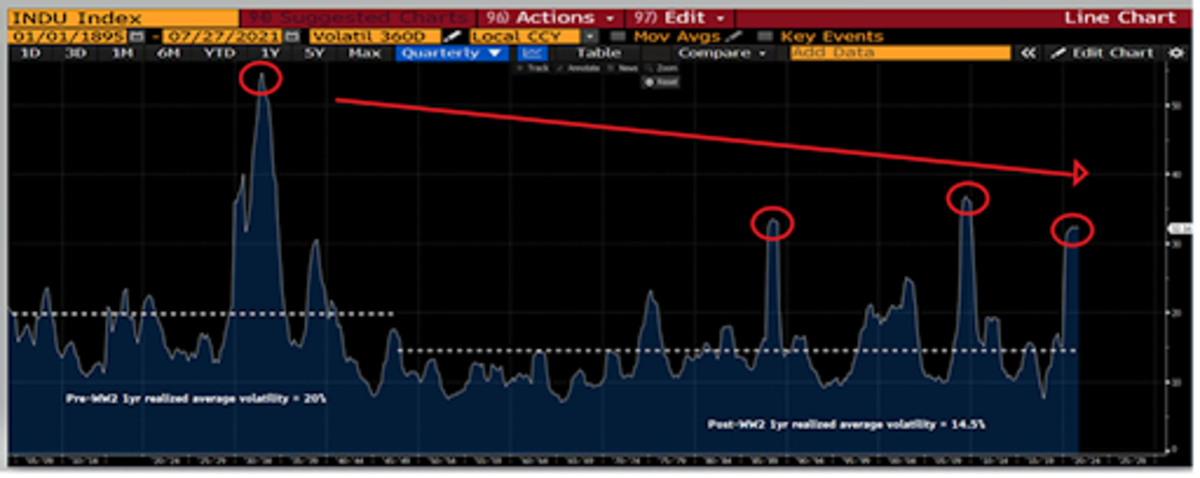

Below is a graph of the realized one-year volatility in the Dow Jones Industrial Index going all the way back to 1895. The pre-WWII average of this proxy for stock market volatility was about 20%, witnessing only one to two “black swan” spikes during a 50-year span. Meanwhile, the post-WWII average has been closer to 14.5%, with three black swan events observed only within a 30-year period!

This graph gives us two important pieces of information:

Volatility is trending lower over time. A move from 20% to 14.5% may not sound significant, but this is a nearly 30% decline in average volatility. The positive effect of such a shift has on underlying asset prices cannot be overstated. A system of declining volatility has come at the heavy cost of greater susceptibility to bouts of near-disastrous black swan events, external and internal shocks. And these events are not capable of being permitted to clear the imbalances that caused them, to self correct, as the system would break before such catharsis could be attained. Instead, each successive crisis forces policymakers to intervene at much lower levels of volatility than in the pre-WWII era. This of course fuels greater abdication of responsibility, which fuels the next crisis as we rinse and repeat, racing toward zero.

Source: @LudiMagistR, Bloomberg

Centralization Is A Fabergé Egg: Systems Which Require Stability And Efficiency Are Always Extremely Fragile

I recently came across a white paper authored by Ben Inker and Jeremy Grantham, famed hedge fund investors at GMO. They conducted a data mining project and looked at the prior periods of frothy financial markets like the 1999 to 2000 period, and similar historic periods of strong performance and excess returns. They were surprised to find that it wasn’t earnings growth, the level of real interest rates, or even GDP growth that mattered during such periods of excess and euphoria.

Instead, they found three consistent variables that were always part of the equation:

Atypically high profitability for one or some segments of the economy (this is finance speak for maximal efficiency rather than maximal productivity)The stability of GDP (as a proxy for overall economic activity)The stability of the rate of inflation

In short, markets care not about actual levels of growth, inflation and profits. Predictability is what matters. A financialized system and a mass investor class requires stability and loathes uncertainty. Said differently, our system of monetary inflation rewards monopoly formation, values efficiency over productivity, and requires reduced volatility to sustain itself.

Given that volatility is a natural phenomenon of any free system, suppressing it requires external and artificial forces. It requires a central authority to manage the system and to solve for low volatility. Our central bank policy of monetizing moral hazard is evidence of this. Moral hazard from this prism is simply a function that solves for low volatility, at all costs. And there are a lot of costs.

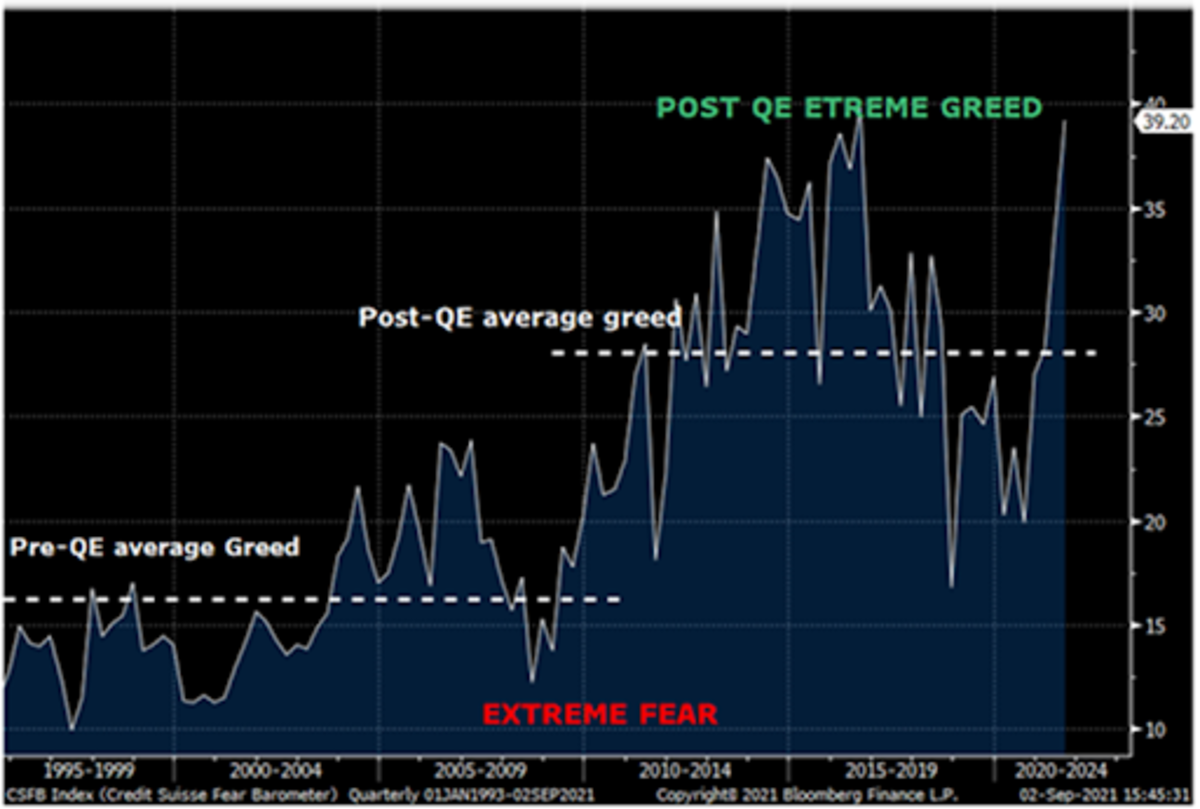

Moral hazard visualized: Credit Suisse Fear And Greed Index. Source: @LudiMagistR; Bloomberg; Credit Suisse

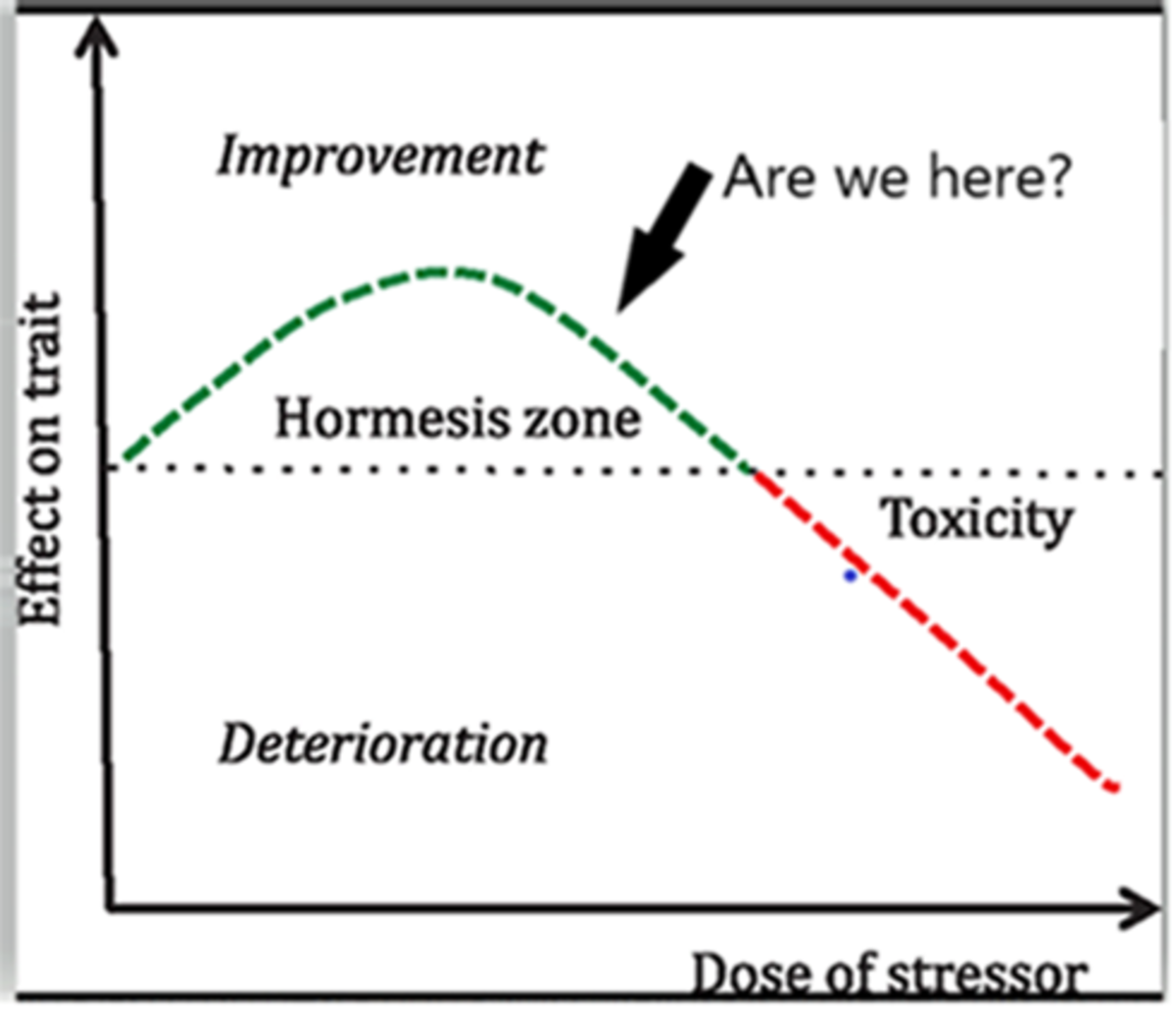

The Difference Between A Medicine And A Poison Often Comes Down To Dosage

While the importance of gains in efficiency are indeed a requisite aspect of technological progress as well as a tremendous generator of wealth for those providing such efficiency gains, there is always a trade off. A great example of this is the Bitcoin block size war of 2017, as well as the many utility protocols proliferating the crypto universe, optimizing for network throughput at the cost of much weaker decentralization. The irony is that the many use cases of blockchains become completely obsoleted without decentralization. Efficiency is great. It’s exciting. It often is associated with innovation. To a point.

Where is this point?

Any marginal gain in efficiency requires a marginal loss of resilience. Given that resilience is vague and incandescent, a decline can seem harmless until it suddenly breaks completely. This means that the relationship between efficiency and resilience is non-linear. There is always a point on the curve where the benefit of efficiency gains become precipitously overwhelmed by the cumulative trade-offs.

Source: Nassim Taleb, “Antifragile”; @LudiMagistR

Ok, fine. Let’s agree that the financial system is in fact becoming more fragile. What does this have to do with centralization of power? Shouldn’t a fragile system lead to the dissolution of power?

Short answer? No.

Less short answer? A centralizing power depends on vulnerability to validate its own existence. As the costs of centralization mount, is becomes existentially vital for an authority to lay claim on the sole ability to medicate the very ailments it fabricates, so as to traverse unstable times unscathed. Fragility maintains power. Power thrives on fragility.

Efficiency Is A Great Barometer Of Where We Are In The Macro Cycle

Why? Efficiency naturally peaks at the end of a regime. By the end of the regime, everyone assumes the cycle to be permanent because no one remembers a different world. We succumb to recency bias, forget history, and inadequately discount the inevitability of change.

Efficiency, fundamentally, is a way of optimizing processes or work to a specific environment. By the end of a regime’s lifespan, an environment’s self-selected economic participants have naturally maxed out adaptations to that one environment, having gone “all in” on its defining characteristics.

Thus, like a grain of sand placed on a growing sandpile, all that is needed is just one inopportune shift and the whole system cascades down with surprising fragility. A meteor hits, and we are cold-blooded, energy-consuming goliaths. Good luck with that!

We’ve of course seen this story time and time again throughout history, both at biological and evolutionary scales when diversity is overcome by uniform specialization, and throughout the annals of human history. This is one explanation as to why empires always eventually fall. Their successes eventually become their weaknesses. Efficiency helps fuel dominance in a world that values power as a function of resources, but it leads to dangerous deficits in resiliency that inevitably make them easy to destroy. This is also why empires are often built over long periods of gradual ascent, but often fall precipitously. Non-linearity.

Thus, somewhat counterintuitively perhaps, periods of maximal efficiency will precede periods of instability and upheaval.

An Obituary For The Private Sector

Now, let us return to volatility.

As the boulder of zero volatility and a fully-managed economy slides precipitously toward its Newtonian fate, there will slowly materialize some incredibly powerful implications for the structure of private property rights. This is because zero volatility and a required real risk-free interest rate held at zero or negative levels will logically push the aggregate cost of capital to extremes.

When there is no risk of material loss for capital, there becomes no discrimination as to how to invest it. The decision-making process becomes tied much more to government policy goals, cronyism and bribery, and other characteristics very similar to those of communist systems of governance. The corporation and the entrepreneur lose their utility in this world.

The birth of the modern corporation can be traced back at least to Adam Smith’s 1776 classic, “Wealth Of Nations,” interestingly published the same year that colonists here in America sought independence.

In this work, he lashed out at the “business association,” his era’s version of the state-owned companies, or the precursor of the “military-industrial” complex, or in China’s case the Sovereign-Owned Enterprise (SOE). These were institutions like the British and Dutch East India companies in Smith’s time.

He argued against monopolist business practices, which in turn paved the way for the legal autonomy of business outside the direct control of the government. As far back as 1844, corporations began earning the status of “personhood,” eventually granting them 14th Amendment rights in 1886. This paved the way for the evolution of corporate oversight toward the domain of the court system and not that of the executive and legislative branches.

The point here is that while we sometimes think of corporations as gatekeepers, monopolists, greedy beneficiaries of consumerism, debt and inflationary growth, these adjectives describe their failures within our current system, not their original purpose. The corporation was originally designed to bestow greater power to the entrepreneur and decentralize power away from the state.

By providing legal protections like limited liability, the corporate structure allowed for individuals to combine resources without unmanageable personal risk, which in turn allowed for the competitive acquisition of capital for investment. So, when the cost of capital and the risk of capital become immaterial, the existential purpose for the corporation becomes difficult to justify. And so the economy centralizes further with the erosion of one more source of decentralization.

What is so exciting about Bitcoin within this context is that it replaces the vacuum created from an impotent corporate private market structure with something much more decentralized and much better suited for the evolving digital information economy. It helps an increasingly interconnected economy divide labor beyond its current stalemate.

Bitcoin is a medium of specialization. Corporations were invented to be a specializing spoke of private capital, allowing for greater and more scalable division of labor. Unfortunately, in a world where the digital realm is becoming the majority sphere of economic activity, where individual property rights had not been assured prior to Bitcoin, the corporation instead has more often become a rent seeker, a bottleneck for competition, and a gatekeeper of digital property. This has had the perverse effect of decreasing our collective ability to specialize. Bitcoin solves this problem.

However, I am getting ahead of myself. We will get into this exciting potential in greater detail in part two of this series.

A Dangerous Cocktail: Why The Pareto Principle Matters

As the world becomes more interconnected, relationships become more “Paretian,” and less “normal,” or mean reverting. This is because the Pareto principle has shown empirically that complex systems often demonstrate extremely asymmetrical distributions of effect. Effects that only magnify as the system grows larger.

Prior to the interconnectedness driven by technologies and the scalability of digital networks, such Pareto effects were only discernible at ultra-large scales or where the complexity of the system was much larger than witnessed in everyday life, in fields such as macroeconomics, astronomy, geology, ecology and theoretical physics. But over time it is being appreciated just how pervasive this Pareto dynamic truly is.

In the business world, it has been shown that roughly 20% of customers often produce 80% of a company’s revenue. Eighty percent of a company’s output, likewise, is often generated by 20% of its employees. The pattern is found in many random systems. Eighty percent of highway accidents occur at 20% of the path traveled (near home), 80% of the cost of building is spent on 20% of the structure, and 20% of the world population is responsible for 80% of the pollution. The list could go on. But this simplified 80/20 rule actually understates the impact, as it is simply an approximate guide, the map rather than the road itself.

In fact, this 80/20 ratio can often turn into 99.9999/.0001 quite easily. Take a simple example where the square root of the total nodes in a given network is the number of nodes that are deemed to have the most measurable impact on that network. If we start with 10 nodes, we have about three nodes fulfilling that role, or about 30%. If the network grows to 500 nodes, we get about 22 nodes, or less than 5% of the network. If we end up with 500,000 nodes on the network, the figure would be about 707 nodes providing that impact, or a stunningly small fraction of 0.1%. Non-uniformity scales exquisitely.

As we begin to see, the Pareto principle is powerful in large systems, and is so important today as the world interconnects exponentially and in increasingly fractal patterns. The bigger the network, the more extreme the variance. Decentralization is a natural outcome of network building, especially if allowed to flourish without interference or external exploitation. Therefore, it is a logical conclusion as a general principle that decentralization increases variance and begins to break down previous patterns of mean reversion that are so characteristic of normal probability distributions.

Conversely, centralization craves more uniformity. Otherwise, there become too many outliers in the herd to corral, and the system becomes unmanageable. As networks proliferate, governments increasingly are driven existentially to ramp up the use of power and coercion against this natural force.

Not only is the world experiencing greater dispersion of outcomes, it is also changing at an increasingly faster pace. Raw data is pouring torrentially down upon us, overwhelming our neural capacity more each day. We are confused, overwhelmed and looking for anchors, answers, and authority.

“Black swan” or “tail risk” events, by definition, are not predictable by any model. Otherwise, they would not be black swans. Models often give us a false sense of stability, understanding, and confidence. The renowned behavioral economist Daniel Kanneman has shown that even when we are given statistical predictions that we know to be spurious, we embarrassingly cannot help but feel assured and make more risky decisions based on such irrelevant data.

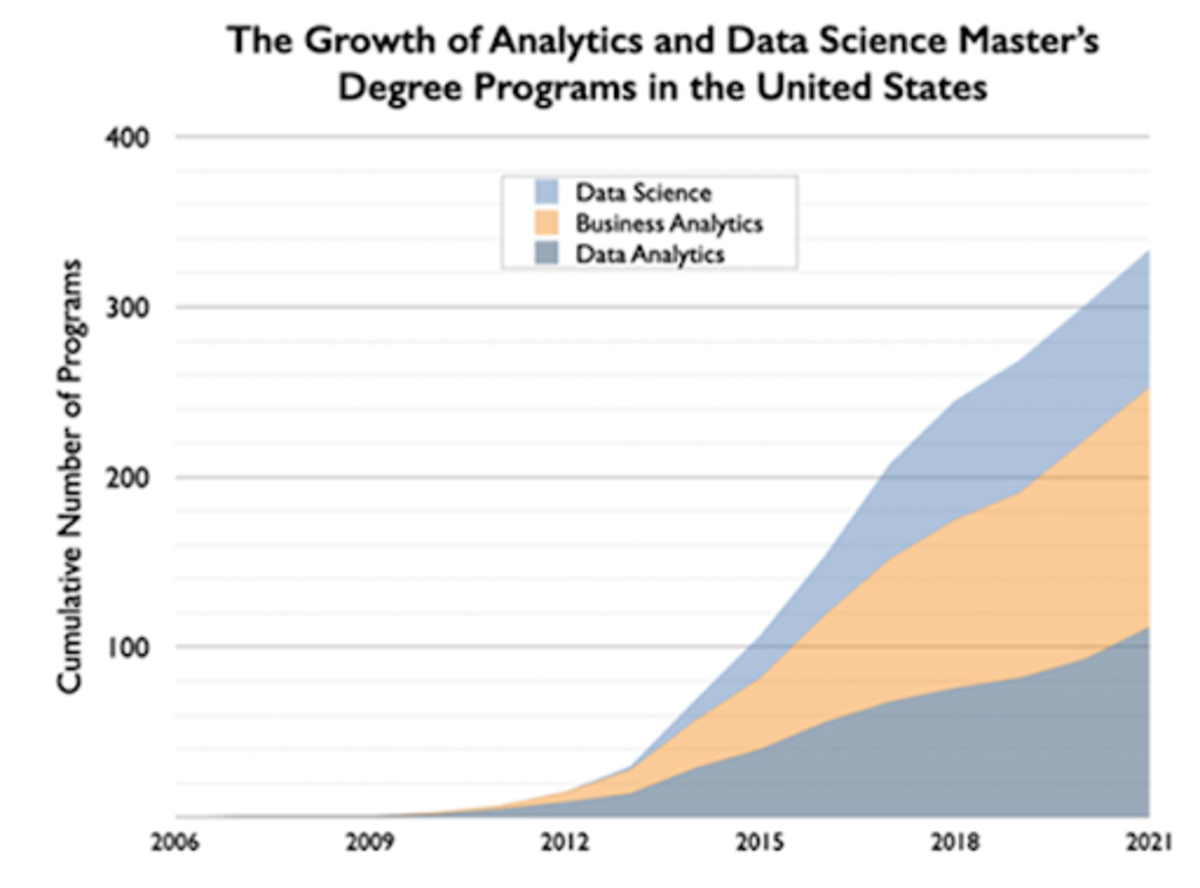

Nonetheless, the pace of change and data dumping has inspired us to overly romanticize and revere data accumulation, prediction, and data modeling techniques. We even have new professions that have popped up to deal with such issues, often aptly referred to as data “scientists.” Most major universities over the past decade have added degree programs for data science and it is now one the fastest-growing programs in academia.

Source: Michael Rappa, Institute for Advanced Analytics, May 2021

Now, let us more holistically recapitulate the situation described above. The cacophony of noise is getting ever louder, and meanwhile, our ability to filter this data to uncover the important signals hiding within has not improved at all.

We have developed technological tools that can filter the raw data and improve its informational extractability. However, these improvements are limited solely to endeavors that we are comfortable deferring to computers to manage for us. In all activities where humans still require involvement or apprehension, we are completely outmatched. On top of this, technology can be a tool, but it can also be a weapon. For every search, storage and AI tool that has helped to unbundle the noise into some semblance of a signal, there are other software tools that re-bundle the signal once again back into noise. Particularly social media, mainstream media, political propaganda and social science professions that overconfidently apply the newfound data abundance.

Taking all of these themes together, we have rampant technological shifts, overwhelming data propagation, and overconfident and confused human actors trying to adapt to these self-inflicted changes to achieve the unattainable: control. This means an increasing risk of the black swan events we so fiercely aim to circumvent. Less predictability, and more hubris as to our collective capacity to pattern-recognize and avoid those rare and historically pivotal events. This is a very dangerous cocktail.

An Homage To Endurance, Tenacity And Immutability

“I think much more likely is an even worse alternative: government will not cease inflating, but will, as it has been doing, try to suppress the open effects of this inflation. It will be driven by continual inflation into price controls, into increasing direction of the whole economic system. It is therefore now not merely a question of giving us better money, under which the market system will function infinitely better than it has ever done before… but of warding off the gradual decline into a totalitarian, planned system, which will, at least in this country, not come because anybody wants to introduce it, but will come step by step in an effort to suppress the effects of the inflation which is going on.” –Friedrich A. Hayek, “The Collective Works of F.A. Hayek,””Toward a Free Market Monetary System.”

Endurance, tenacity and immutability. While these attributes may sound too passive or unsubstantial to have value in our “move fast and break things” world, they are the exact traits required to survive the fragility of a system dashing feverishly towards instability.

Antifragility, an idea popularized in the 2012 book “Antifragile” by Nassim Taleb, describes systems or phenomena that gain strength from disorder. This book, part of a larger work focused on philosophical, statistical, and economic misconceptions relating to systemic risk, uncertainty, and randomness, has become part of the larger canon of Bitcoiner manifestos. This is despite Taleb’s recent baffling divorce from the community, which while a tad perplexing, should not detract from some of his work’s takeaways.

Bitcoiners have latched onto the themes of “Antifragile” as a framework to help elucidate some of Bitcoin’s game theory. How is it that there is no silver bullet that kills Bitcoin, there is no competitor that can magically overtake it, there is no government that can shut it down, and there is no central authority that can censor or confiscate it?

But the message does not stop there. Most important to the thesis of antifragility, each attack vector and shock to the system in fact causes Bitcoin to become stronger.

As Taleb writes:

“Some things benefit from shocks; they thrive and grow when exposed to volatility, randomness, disorder, and stressors and love adventure, risk, and uncertainty. Yet, in spite of the ubiquity of the phenomenon, there is no word for the exact opposite of fragile. Let us call it antifragile. Antifragility is beyond resilience or robustness. The resilient resists shocks and stays the same; the antifragile gets better. This property is behind everything that has changed with time: evolution, culture, ideas, revolutions, political systems, technological innovation, cultural and economic success, corporate survival, good recipes (say, chicken soup or steak tartare with a drop of cognac), the rise of cities, cultures, legal systems, equatorial forests, bacterial resistance … even our own existence as a species on this planet. And antifragility determines the boundary between what is living and organic (or complex), say, the human body, and what is inert, say, a physical object like the stapler on your desk… The antifragile loves randomness and uncertainty, which also means — crucially — a love of errors, a certain class of errors.”

We have seen firsthand how the market can reward an asset that exhibits antifragility. Astute macro investor Louis Gavkal has wisely observed that this is how the U.S. treasury market has evolved.

Today, investors have institutionalized portfolio management, packaged into strategies like 60/40 asset allocations (bonds/stocks), and slightly more volatility-adjusted strategies such as risk parity. However, this love affair with the treasury market as a diversification tool has not always been the case, especially from the perspective of global investors. In fact, treasuries may be losing this status. The godfather of risk parity, Ray Dalio himself, just recently confirmed the view that he would rather own bitcoin than bonds.

What has historically given treasuries their stature of primacy for so many years was the dollar’s reserve currency role. A feat attained through war, geopolitical victories, petrodollar arrangements, and the trade-offs of increasing consumerism and domestic debt accumulation in the U.S. to supply dollars abroad. All punctuated by a parallel hyper-financialization of our economy, with regulatory incentives to own treasuries and a global system addicted to dollar-based leverage and short of adequate collateral.

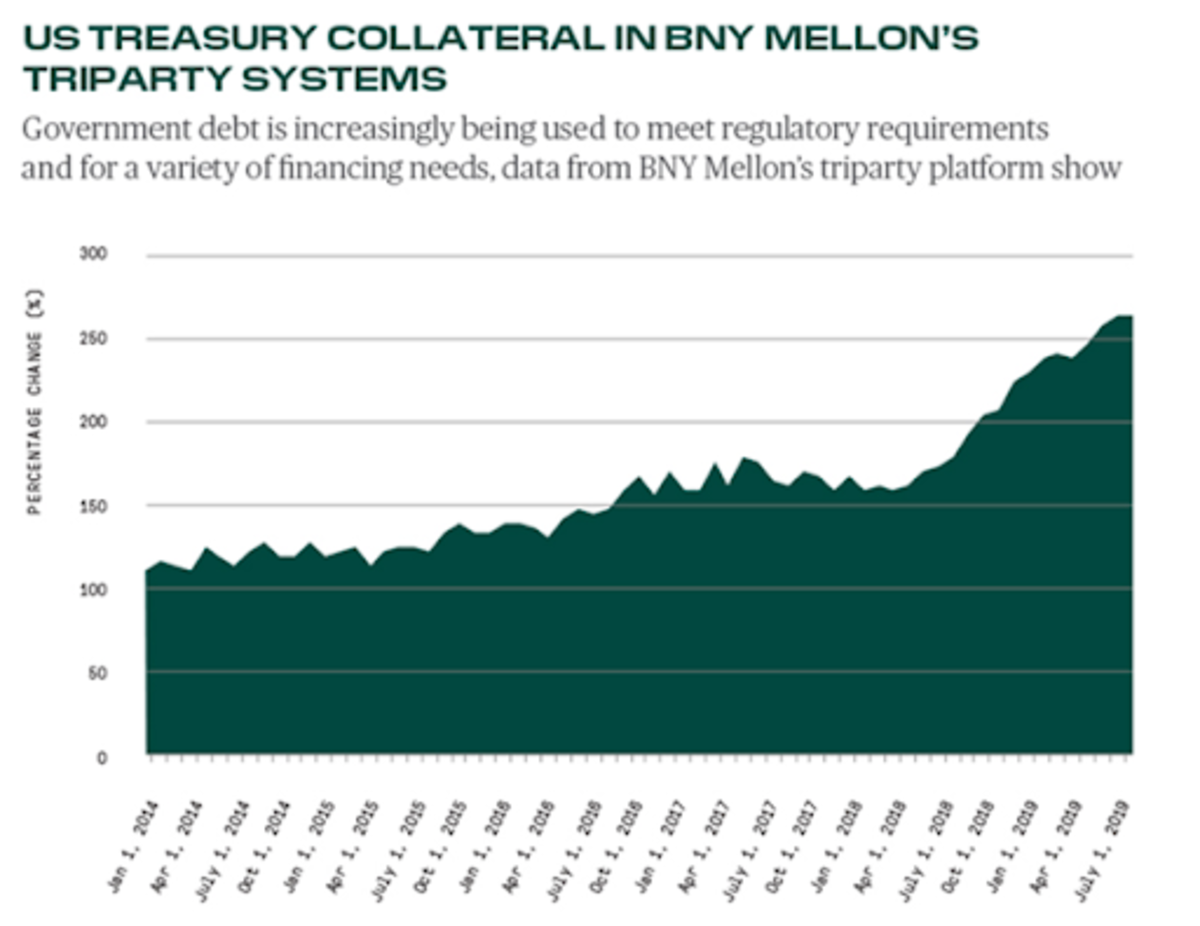

This collateral shortage has become particularly acute after quantitative easing has been significantly reducing the public supply of treasuries since 2009. All of these factors have helped create a treasury market monster with very resilient network effects for the U.S. dollar. Resilient to deleveraging elsewhere, resilient to market volatility, resilient to dollar shortages, and even resilient to cyclical inflation.

The treasury market is a massive battleship that has been chugging along full steam in one direction for many years. However, this ship is now altering its course. And this process is ever so slowly chipping away at those network effects. As the U.S. dollar necessarily loses some strength as a reserve money, the system will either need to deleverage or find a new source of collateral, a new antifragile asset.

Source: BNY Mellon

One way to think of the U.S. treasury market’s ability to maintain buyers and holders despite real interest rates, at least at negative 1% (depending on your gauge of inflation), is that this market has become a weigh station, a storage space for dollar-denominated assets, intended to balance existing portfolios of dollar-denominated equity, real estate and corporate debt holdings, as a reserve account that incentivizes participants to remain within the bounds of the existing USD ecosystem.

The Eurodollar system, U.S. dollars banked or held outside of the U.S. banking system, evolved to help accomplish this goal more efficiently at the global level.

The Eurodollar market size has exploded as the U.S. economy began to financialize in earnest: First in the early 1980s and then again in the 1990s and post-dot-com burst.

The start of this in the early 1980s coincided with the start of a 40-year bull market in U.S. treasuries:

Source: Federal Reserve Board

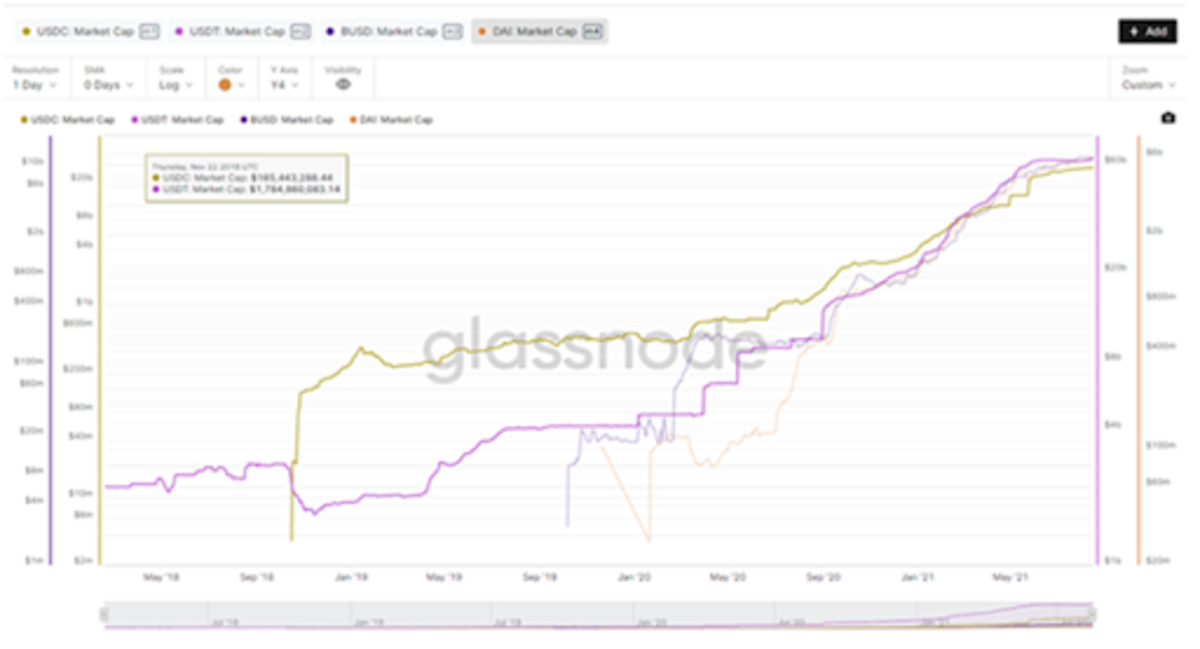

Such a concept of captively on-ramped capital is actually very similar to the stablecoin market in the Bitcoin and cryptocurrency ecosystems.

Source: @LudiMagistR; Glassnode

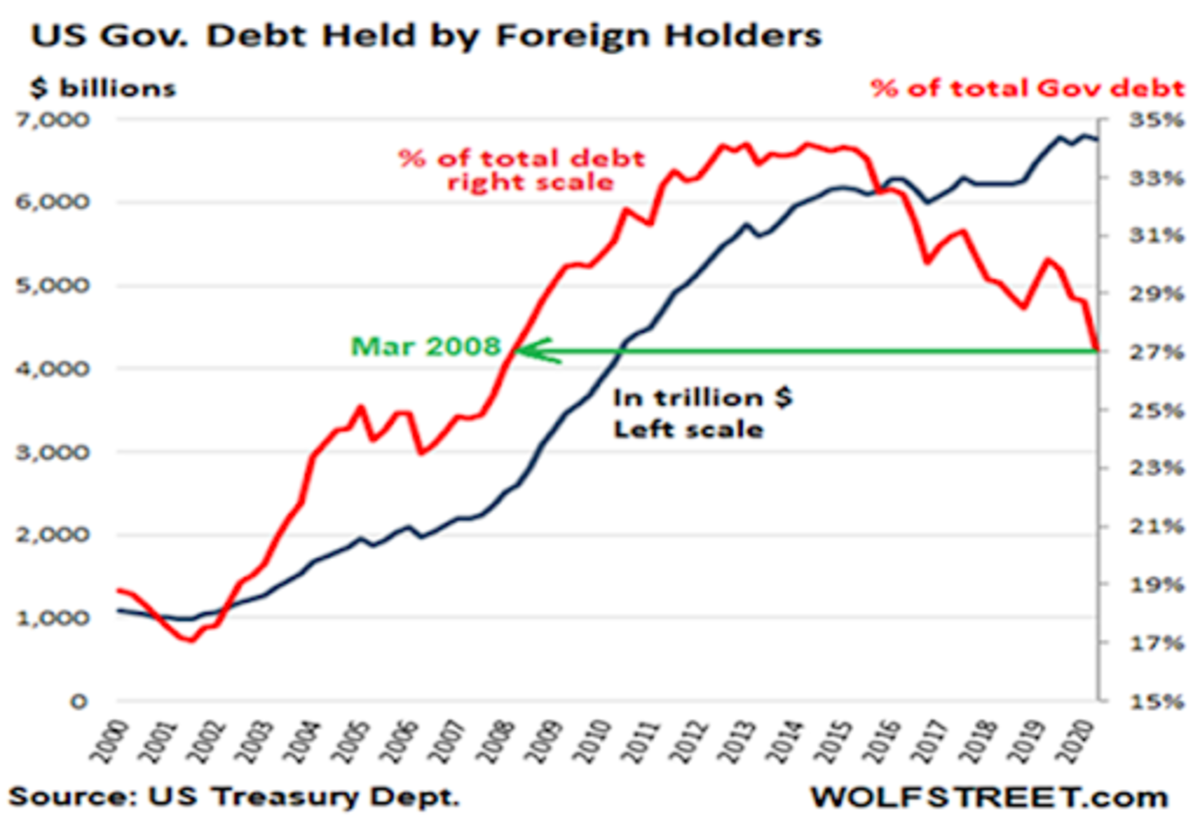

Unfortunately, for the U.S. dollar fiat ecosystem, there are signs of deterioration within its network effect. Foreign users are balking.

Source: Wolfstreet.com

A Poetic Phrase: Bitcoin Is A “Deep Structure”

“In a Paretian world, surface events can become a distraction, diverting attention from the deep structures molding these surface events. Surfaces are extraordinarily complex and rapidly evolving while the deep structures display more simplicity and stability. These deep structures are profoundly historical in nature — they evolve through positive feedback loops and path dependence. Snapshots become misleading and understanding requires a dynamic view of the landscape.” –John Hagel

We live in a world where things are intentionally made to fall apart. Quantity and popularity are valued above quality and depth. The news cycle is a meager 24 hours. Medical and health problems are addressed ex post facto with newly-invented medications and treatments, rather than by way of lifestyle changes and preventative measures.

Products are meant to become obsolete. Buildings are designed to last 20 years rather than 200. Tweets share ephemeral memes instead of lasting ideas, investments are made for instant return potential rather than lasting productive impact. And interest rates have collapsed to near zero, allowing us the mathematical permission to discount the future so that it is indistinguishable from the present.

We have lost our ability to think long term. We have no appreciation for durability over time. Therefore, we do not particularly value persistence because its main attribute is indeed durability over time.

Taking this a step further, if we do not place any material value on resilience, how could we value antifragility at the societal level? This is because antifragility is simply resilience in the form of a productive asset. By this I mean something that is durable, but also something that improves over time. It is no wonder then, that even Bitcoiners may be undervaluing antifragility.

This irony is further extended by the fact that just at the time when civilization least values such a high-powered form of durability and productivity happens to also be when these attributes are most desperately needed.

“An Ocean’s Ode To Volatility”

Oh waves, Crash thunderously

Unshackle my bounty of lost minerals

So they may rise and greet my surface foam

Antifragility is an embrace of volatility.

Volatility is the mathematical expression of what biologists and evolutionary scientists might call a “stressor.” Biological organisms crave stasis. Volatility, on the other hand, is a natural characteristic of all complex systems. This is because the greater the number of variables, the greater the number of possible outcomes. Stressors lead to adaptation and growth, which leads to survival, which builds resilience, which lays the foundation for more resilience and growth.

It is a positive compound growth formula because the more resilient we get, the more volatility we can swallow, without choking on it. As implied above, an increase in volatility can be thought of in this context as just a greater range of circumstances. But this can come from two sides, like a matrix of potential outcomes.

On one axis, you have a quantity and variety of stressors, but on the other you also have a quantity and variety of reactions, responses and results. In a decentralized system, both axes expand over time, generating an exponential function as two growing variables are multiplied by one another. When systems lack a centralized gatekeeper, more stressors are allowed to propagate. Likewise, there is greater diversity and heterogeneity of participants that can react uniquely to these stressors.