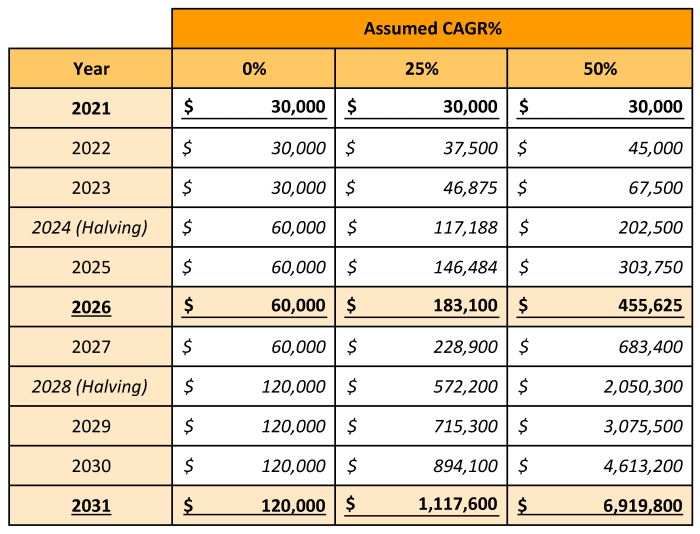

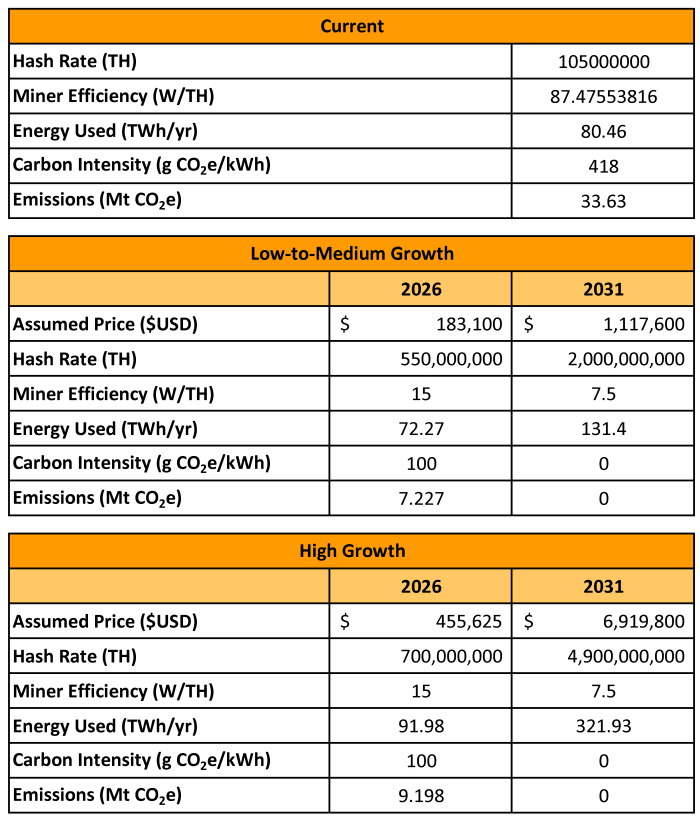

Let’s assume the absolute worst of the above performance results, the four-year annualized growth rate, about 50%, and halve it. This results in a price of $183,000 in 2026, and $1,118,000 in 2031, a market cap of around $23 trillion.

Scenario Three: 50% Annual Growth In Daily Demand

Since we assumed the worst of the long-term performance results above, this time, we will still assume so, but not halve it, and just go with a 50% annual growth rate. This results in a price of $455,000 in 2026, and $6,920,000 in 2031, a market cap of about $140 trillion.

Hash Rate And Technology Assumptions

In June 2018 (page nine), I compared the latest miner at the time, the Bitmain Antminer S9i, with the leading model in January 2015, the Antminer S5. In that 18-month period, ASICs increased their efficiency nine-fold, consuming only 98 watts per terahash (W/TH), down 89% from 890 W/TH in 2015. Three years on, and the Antminer S19j Pro achieves 29.5 W/TH, a further 70% reduction in energy. Although the aforementioned chip shortage will most definitely stifle supply dramatically for at least two more years, innovation will not be stifled, and I would assume an efficiency of 15 W/TH in 2026, and 7.5 W/TH in 2031.

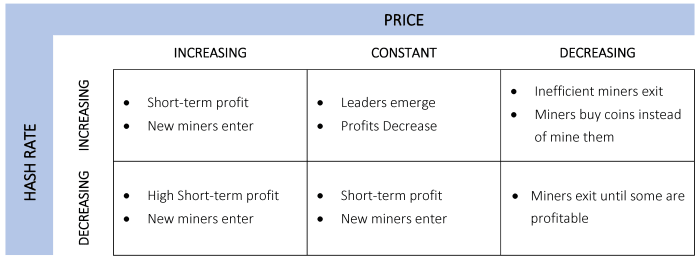

In terms of overall hash rate, average growth rate has been on a downward trend for several years, while volatility in growth rate has been on an upward trend. This could be due to recent production and supply issues, seasonal migrations or that the installed base of ASIC miners is now so large that the marginal additions from new production are becoming less significant.

If the latter isn’t the case already, it likely will be in 2026, and most definitely will be in 2031. Anything more than average growth of 1% per difficulty epoch would be highly unlikely. That said, hash rate does follow the price, and if price is growing that dramatically, perhaps supply would appear. But, with even a “small fab” costing in the order of $12 billion and taking eight years to complete, it’s hard to see hash rate growing more than 1% per epoch regardless of price, certainly not for another two or three years. Perhaps in a “scenario three” situation where price rises so dramatically that chip producers will be compelled to prioritize the Bitcoin mining industry due to the sheer profitability, we may start to see extraordinary average fortnightly growth.

I will assume that by the end of 2021, all hash power evicted from China will be back online in another jurisdiction, and the year will end at a hash rate of 150 exahashes per second (EH/s). Assuming price growth scenarios one and two (0% and 25% per year, respectively), 1% growth rate in hash power every difficulty epoch is assumed. This gives us around 550 EH/s in 2026, and 2,000 EH/s in 2031.

In the case of scenario three panning out, we will assume 1% until 2024, and 1.5% from 2024 onwards on account of the resolution of the chip shortage and prioritization of the Bitcoin mining industry due to very high profitability. This gives us around 700 EH/s in 2026, and 4,900 EH/s in 2031. The key takeaway is that no matter how far price outstrips hash rate due to production limitations, the gap will be bridged through a natural increase in ASIC prices. In perfect competition, CAPEX + OPEX will always tend to the price of a bitcoin — no matter what.

On a separate note, a slow growth in hash power has the added benefit of equipment becoming obsolete much slower, extending equipment life, hence reducing environmental load.

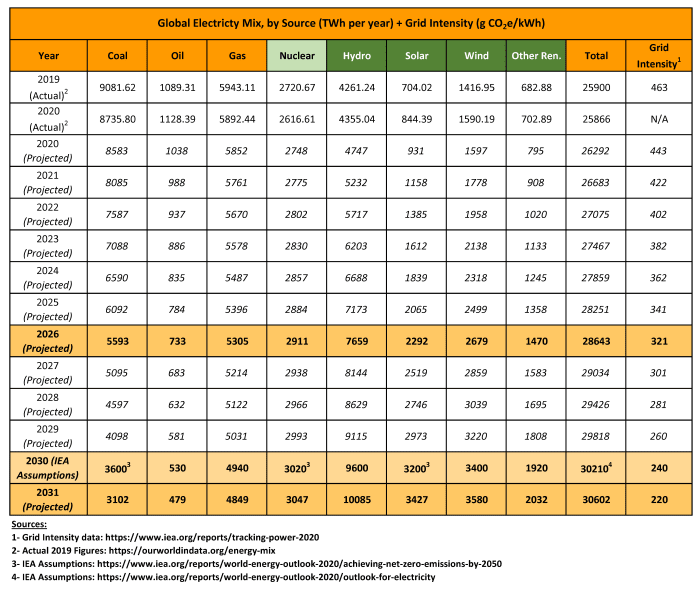

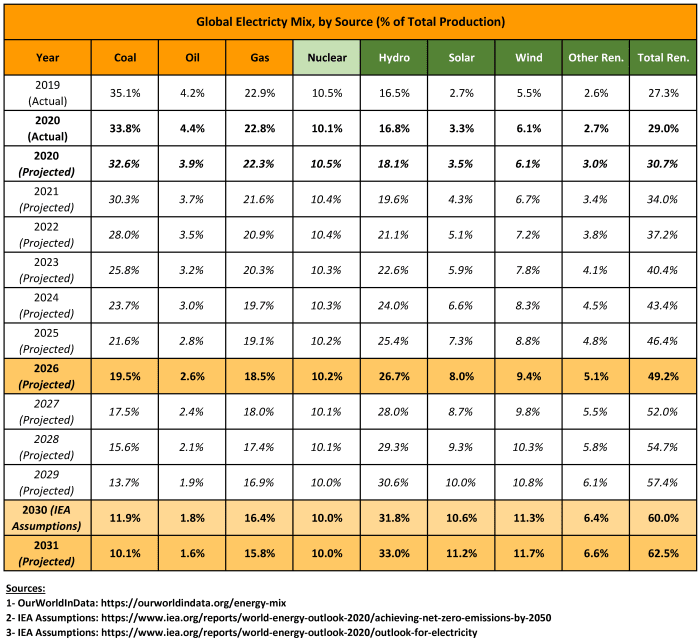

Energy Mix And Price Assumptions

No need to make too many guesses on this one, the International Energy Agency (IEA) already has its 2030 targets in place in its “2020 Energy Outlook.”Here are the highlights:

“Primary energy demand in the Net Zero Emissions by 2050 (NZE2050) scenario falls by 17% between 2019 and 2030. Coal demand falls by almost 60% over this period to a level last seen in the 1970s. Emissions from the power sector decline by around 60%. Worldwide annual solar PV additions expand from 110 GW in 2019 to nearly 500 GW in 2030, while virtually no subcritical and supercritical coal plants without carbon capture (CCUS) are still operating in 2030. The share of renewables in global electricity supply rises from 27% in 2019 to 60% in 2030, and nuclear power generates just over 10%, while the share provided by coal plants without CCUS falls sharply from 37% in 2019 to 6% in 2030.”

Accounting for all of the above, we will assume a linear improvement from 2019 to 2030 to extrapolate the world average energy mix and intensity in 2026 and 2031, as shown in the tables below.

Since Bitcoin is currently cleaner than the world average grid (418 g versus 463g CO2e/kWh), and considering the China ban, Bitcoin is currently very easily over 50% total renewables, also known as “The Elon Threshold.” I predict that due to offset emissions from prolific use of flared methane to mine bitcoin, as well as Bitcoin being agile enough to move to the cheapest (i.e., cleanest) energy sources — whether it is a remote oil field or volcano — the carbon intensity of Bitcoin in 2026 will be 100g CO2e/kWh, and by 2031 it will be zero (or negative).

Energy Use And Emissions

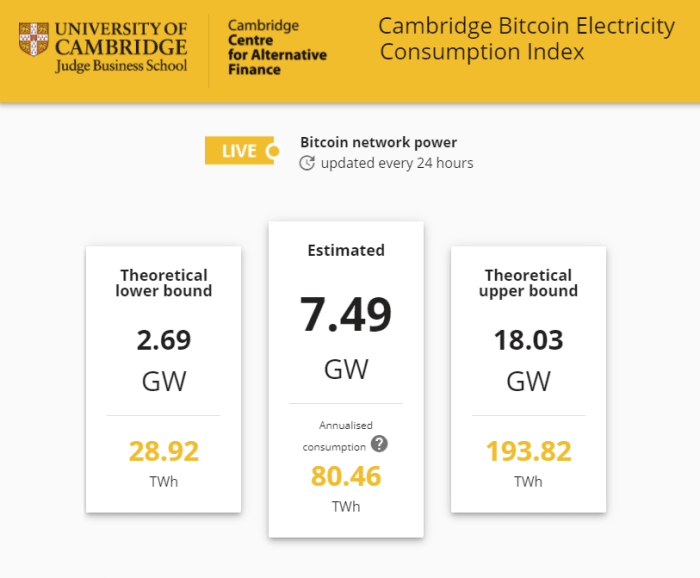

We now have the following two scenarios, the associated assumptions and their final energy use and emissions. Current data is based on cbeci.org, as at June 23, 2021, per the screenshot shown below.

From the above, it would appear that Bitcoin’s emissions peaked a few months ago, and thankfully, with the banning of Bitcoin mining in China, has commenced its aggressive march down to zero emissions. It is expected that in the worst case, emissions from Bitcoin in five years will be less than a third of its emissions today, and in 10 years, Bitcoin will emit nothing at all.

While this may seem counter-intuitive, when all of the data is aggregated and assessed with logic and textbook business and economic frameworks, it can be easily seen that Bitcoin poses almost no threat to the environment. Indeed, in the best case, Bitcoin will actively heal the environment through offsetting of flared methane and by holding the key to an abundant, clean energy future. I look forward to revisiting this prediction in 2026!

This is a guest post by Hass McCook. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

2016年から

2016年から